Last Updated on October 10, 2023

In this part – how to fill out Anlage Wa-Est.

Anlage Wa-Est is filled out by those

- who left Germany in the declared year,

- who moved in Germany in the declared year

- but also those who do not have a permanent place of residence in Germany, but would like to be treated as unrestricted taxable (that is, as living in Germany).

All I can return from tax: A-D, E-H, I-N, P-W

Anlage N Part 1, Part 2, Anlage N-Aus, Anlage Wa-Est, Homeoffice

Anlage Kind

Anlage Vorsorgeaufwand

Anlage Sonderausgaben

Anlage Haushaltnahe Diensleistungen 35a

Who should file a tax return in Germany

Pre-filled declaration in Elster

How to calculate tax in Germany. What is written in Berechnung in Elster

Freiberufler in Germany: how to fill in Anlage S and Fragebogen zur steuerlichen Erfassung

Let me remind you that I am not a professional tax consultant. Declarations are considered from the point of view of an ordinary user: a family with children and one working person of average income.

How to fill out Anlage Wa-Est application

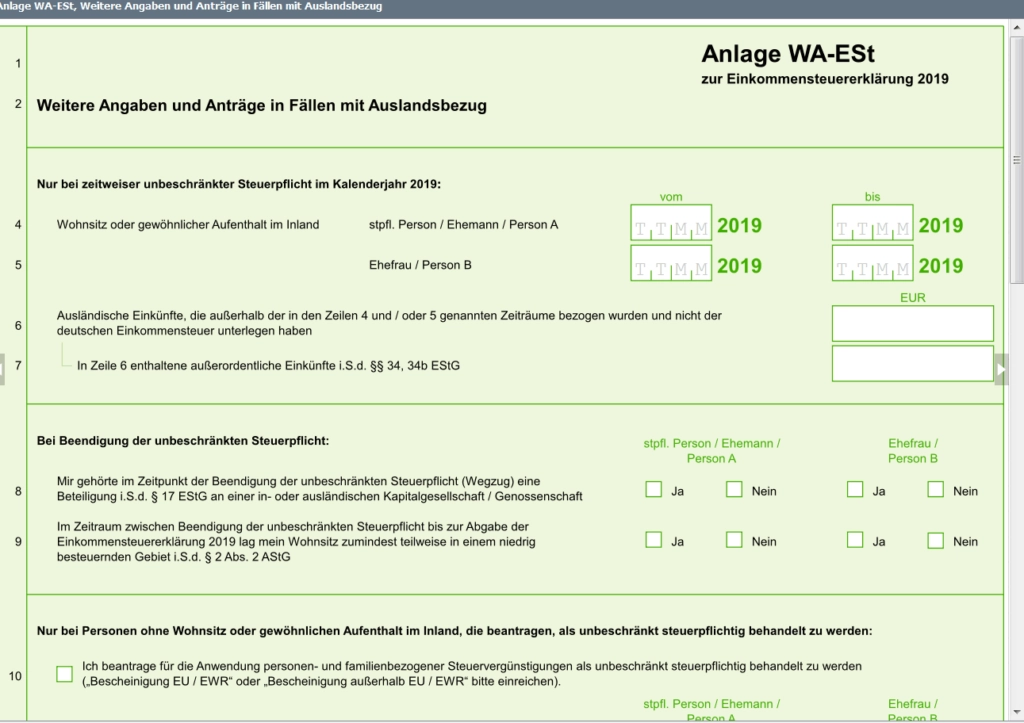

This application looks like a simplified tax return.

Most typical expats moving to Germany in the declared year need lines 4-6 and lines 18-19.

Line 4 and 5 – period of stay in Germany for partner A and B

Line 6 – income abroad. Einkünfte supposes gross income minus Werbungskosten. Expenses are deducted according to the same rules as in Germany.

For the Werbungskosten, it is recommended that you include an explanation of which costs you wish to deduct.

See what you can deduct as Werbungskosten – All I Can return topic (mostly part 4 Work’s expenses).

Line 7 – außеrordentlichen Einkünften. Extraordinary income includes capital gains from the sale of businesses, from agriculture and forestry, commercial operations or self-employed work, compensation, user payments and interest, provided that they have been paid for more than three years.

Zu den außеrordentlichen Einkünften zahlen Veräußerungsgewinne aus der Veräußerung von Betrieben, Teilbetrieben, Mitunternehmeranteilen, die unter die Einkünftsarten Land- und Forstwirtschaft, Gewerbebetrieb oder selbstständige Arbeit fallen.

Hinzu kommen Entschädigungen, Nutzungsvergütungen sowie Zinsen, sofern sie für ein Zeitfenster von mehr als drei Jahren ausgezahlt wurden. Zu guter Letzt zahlen zu den außerordentlichen Einkünften Vergütungen für mehrere Tätigkeiten, sofern sie sich über mindestens zwei Veranlagungszeitraume erstreckt und einen Zeitraum von mehr als zwölf Monaten umfasst haben.

Lines 8-9 are for those who left Germany.

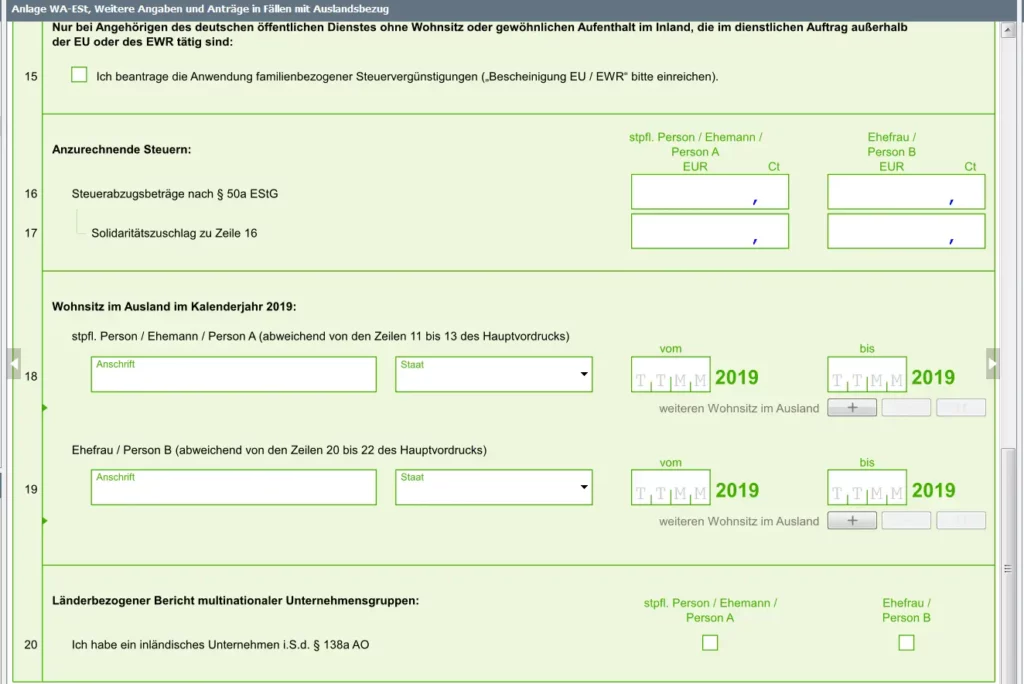

Lines 10-15 – for those who want to be taxed as living in Germany, but not living in it.

Line 16-17 – for Vergütungsgläubiger. This does not apply to ordinary expats

Lines 18-19 are the address abroad and the period of stay there.

Other posts about german tax return – #steuererklaerung.

Do you enjoy the site without cookies and maybe without ads? This means that I work for you at my own expense.

Perhaps you would like to support my work here.

Or Cookie settings change: round sign bottom left

Thank you, it was a good help.

Thanks! Very helpful.