Last Updated on September 26, 2023

Briefly about who should file a tax return in Germany, I wrote in the introduction to the topic on filling out a German income tax return. But there was no answer to the question:

I came in Germany this year

I am employee and have no other income

– should I file a declaration in Germany for this year?

In the list of those who must file a tax return in Germany, there are no fresh arrivals in the country. But my old memories of working for a tax magazine brought to the surface a vague knowledge of tax residency. Let’s try to understand this difficult topic, but first we will find out who is still on the list of those who must file.

Child expenses in Germany in October 2022

And you thought you were being praised. German certificate of employment Arbeitszeugnis

How to change health insurance in Germany

Credit cards in Germany

What is Girokonto in Germany

Germany apartments search. Decoding ads

Tax return in Germany. Elster online. Mantelbogen, or Hauptvordruck

Pre-filled declaration in Elster

Freiberufler in Germany: how to fill in Anlage S and Fragebogen zur steuerlichen Erfassung

Please note that I am not a tax advisor and am not responsible for your return. The topic of income in different countries is extremely complex, since there are many details for each country. If your case is complex, if you are not sure and are afraid of making a mistake, contact a specialist. You can choose between Lohnsteuerhilfeverein and Steuerberater. The second option is more expensive, but covers cases that the first does not.

Who must file a tax return in Germany

The tax authorities are interested in your income, so everything is quite simple:

- you have one source of income and it itself submits data to the tax office – you do not have to do anything,

- you have more than one source of income (for example, your wife has also an income) – the tax office is not able to keep track of all of you here, so please submit the data for yourself

- you yourself or your only source of income went beyond the standard scheme (asked for a tax rebate, paid non-standard income) – of course, you must report this

What happens with the deduction of expenses – the tax office does not care, but it should worry you, so many people file a declaration voluntarily and receive some of the taxes back.

How much “some of the taxes” is impossible to predict in advance, because there are too many options. The deductions will depend on tax classes, distance to work, number of children, and many other circumstances. Therefore, the example of other people cannot be a guide: it is almost always beneficial to file a declaration voluntarily, but only the declaration itself will determine how profitable it is.

You must

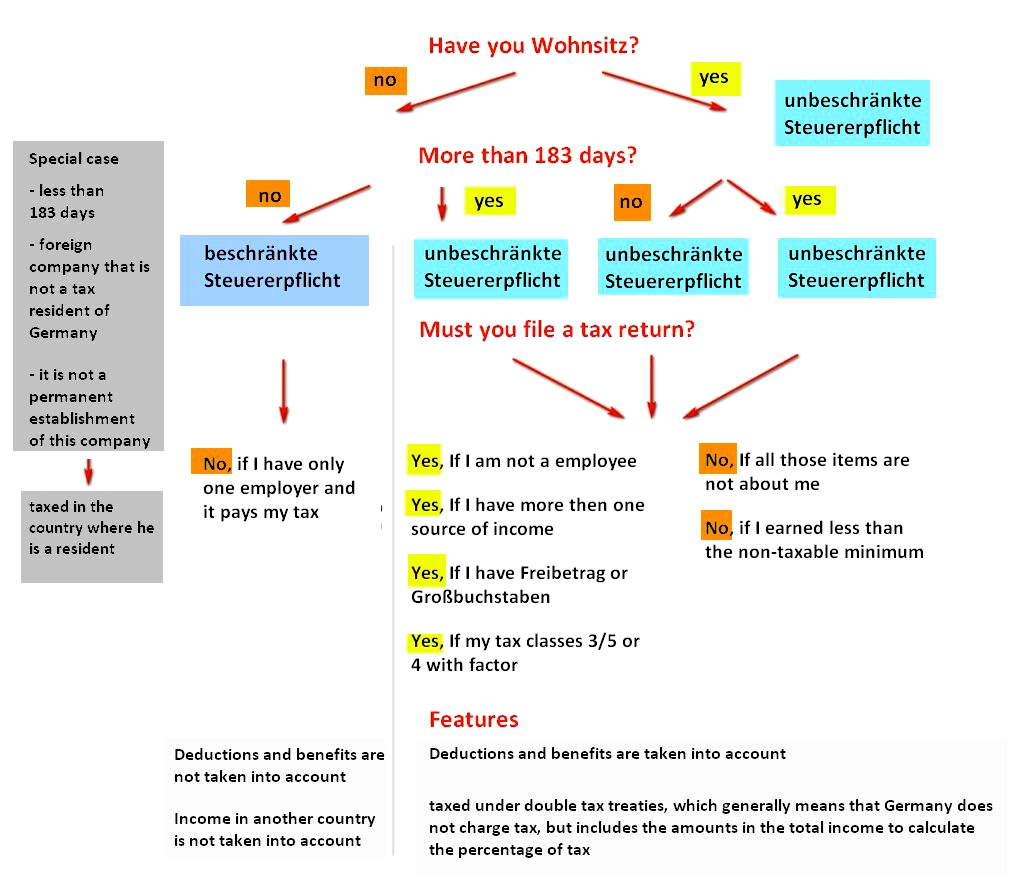

1. Families in classes 5 and 3, if the partner in class 5 receives more than 410 euros of income per year, or families in class 4 with a factor. These classes imply approximate taxation – there may be an underpayment of tax, and an overpayment, so a recalculation is necessary.

2. Those who have a second job (class 6) or other source of income more than 410 euros per year – renting out, or solar panels on the roof / balcony, or working as a photographer, or investment income (if it has not already been banked), or…

3. Those who received compensation for the loss of earnings from the state – Lohnersatzleistungen. These are childcare benefits (Elterngeld), long-term sickness benefits (Krankengeld), job loss benefits (Arbeitslosengeld) or work reduction benefits (Kurzarbeitergeld). Since payments are made by other organizations (for example, Arbeitsamt) – you have two sources of income.

4. A provisional tax reduction (Freibetrag) was requested. This is done when a person does not want to receive deductions for certain items later, but wants to immediately reduce the amount of taxes. Naturally, the Finanzamt still wants to know how legitimate this desire was and how much taxes need to be adjusted. Exception: the disabled, left without care and single mothers who receive a lump sum discount.

5. You received some extraordinary payments from the employer: upon dismissal by agreement of the parties, for example (Abfindung) or compensation for several years (Vergütung für eine mehrjährige Tätigkeit).

6. You have letters in the line “Großbuchstaben” in Lohnsteuerbescheid.

7. You applied for a loss carry-forward to the next year (Verlust).

8. Individual entrepreneurs (freiberuflich / gewerblich)

Tax residents and tax non-residents: limited taxation and the 183-day rule

So, we do not see a direct indication: “you are obliged if you came to the country this year.” However, there is a suspicious item 2 – other income is more than 410 euros. Does this apply to the Finanzamt if I received income abroad before I moved? What if I only lived in Germany for a month?

Who is tax resident

As a resident (ansässig) countries usually considers a person:

– if he has a place of permanent residence in it

– if he has places of permanent residence in two countries – the place where the center of vital interests is located

– if he does not live in either of the two – the one whose citizenship he has

– if it is impossible to determine by citizenship – then by agreement of the parties

Germany distinguishes between Wohnsitz – place of residence and gewöhnliche Aufenthalt – permanent residence if a person stays in Germany for more than six months within 12 months. Leisure trips or visits do not count.

Who files a limited declaration – Beschränkt steuerpflichtig

A limited declaration only for income received in Germany is submitted by those who do not have a Wohnsitz residence and who have been in Germany for less than six months.

Here the first point is more important – whether or not there is a place of residence. Only having determined the first point and having received a negative answer to it, can we move on to the second point. If the answer is no, then taxation is limited.

Wohnsitz has such a vague definition that it is only possible to understand what exactly was meant by examples. Based on the examples, those do not have Wohnsitz, who come to do occasional jobs with no intention of staying. For example, a person came for 2-4 months, rented an apartment, did the work and left. What type of apartment he rented does not matter. The purpose matters – temporarily.

If you only have Wohnsitz for two months this year, but intend to live in Germany for several years, then you are already considered unbeschränkt steuerpflichtig. The same applies if you have two places of residence in different countries and regularly return to the place of residence in Germany. And even if you were going to work in Germany for a long time, but the contract was terminated – you are still unbeschränkt steuerpflichtig. Germany interprets all doubts in favor of full taxation.

Therefore, those who arrived in the second half of the year and, accordingly, lived in Germany for less than 183 days, but concluded a contract and intend to stay further, are subject to unbeschränkt steuerpflichtig.

Those who leave at the beginning of the year but have spent more than 183 days in Germany during the previous 12 months are also subject to full taxation. Even two days in the new year is enough for this. This is called zeitweise unbeschränkt steuerpflichtig and is equivalent to the usual full taxation.

At the same time, Germany considers 183 days quite freely. If you went on vacation for a couple of weeks, then this is not considered an absence and is not taken into account.

But is it even worth striving for beschränkt steuerpflichtig? This limited taxation does not take into account your income in other countries, but it does not take into account your expenses. In this case, the tax-free minimum is not taken into account, numerous deductions and benefits are not taken into account.

Therefore, those beschränkt steuerpflichtig who have more than 90 percent of their income earned in Germany or whose other income does not exceed the tax-free minimum can request full taxation.

Double tax treaties

You are unbeschränkt steuerpflichtig. It means, you has to inform German tax office about all your income also in other countries. Will Germany take taxes on income received in other countries? To answer this question, you need to find out whether a treaty was concluded with the country where these incomes were received to avoid double taxation. These agreements define who will milk the client.

Germany has agreements with about 70 countries of the world, including Armenia, Azerbaijan, Belarus, Estonia, Georgia, Israel, Kazakhstan, Kyrgyzstan, Latvia, Lithuania, Moldova, Russian Federation, Tajikistan, Turkmenistan, Ukraine, Uzbekistan.

Unfortunately, the treaties are not exactly the same, so each must be studied separately. The key point is the 183-day rule (half a year with a one-day margin).

But here, too, the rules are not the same. Some countries count 183 days of a person’s physical stay in the country, including the days of departure and arrival. Others count only days of actual work in the country. Some count according to the calendar year, others according to the tax year (which does not coincide with the calendar), others simply 12 months.

Treaties generally cover:

income of individuals and profits of enterprises

including income from the use of real estate

royalties

dividends and interest

Let’s consider the item on income from employment, since it concerns the majority.

It could be formulated like this:

– income is taxed in the country where the work is performed

– but this is not taken into account if the resident spent less than 183 days in the country during any twelve months beginning and ending in the relevant tax period and worked for an organization that is not a resident of the country where he worked, and not for a permanent establishment of this organization

If there is no double tax treaty, then all income of the taxpayer subject to full taxation will be taxed as German.

Conclusion

And where is the answer to the question, is there an obligation to file a declaration?

The answer is nowhere directly given, but follows from the above.

You came to Germany with the intention of staying for a long period, signed a contract with the employer and rented an apartment. It doesn’t matter if it was in January or December – you are zeitweise unbeschränkt steuerpflichtig, that is, subject to full taxation.

With full taxation, the German tax authorities are interested in all your income for the entire year – the type of taxation applies to the entire year, even if you were owed two days during the year.

According to the second item on our list at the beginning of the article, you must file a declaration if you have more than one source of income during the year. You had income, for example from an employer, in your country and there is income in Germany, that is, you should file a tax return. If you did not receive income in the country of origin this year, then there is no obligation.

Follow me

Another thing is that income in another country will not be subject to German taxes under double tax treaty. But it will increase the amount of income for the year, which will affect the tax percentage that will be taken from you.

Income in another country is reflected in the Anlage Wa-Est application. You can reduce them by the same Werbungskosten as in Germany.

Anlage Wa-Est

German income tax declaration. Anlage N-Aus

Elster online. German income tax declaration Anlage N. Part 1

Tax return in Germany. Elster online. Anlage N. Working expenses

All income tax deduction (in German tax return)

All posts about #finance

All posts about #German tax return

Do you enjoy the site without cookies and maybe without ads? This means that I work for you at my own expense.

Perhaps you would like to support my work here.

Or Cookie settings change: round sign bottom left