Last Updated on January 21, 2023

An account in Germany is the most important thing to do after moving, because all current payments here go through an account called Girokonto.

This topic is about what is giroconto, what is important for choosing giroconto, and also about what other accounts there are.

Credit cards in Germany

What is allowed to do if you are sick without to be fired

Germany by car. Basic information

Health insurance. 1. What is GKV. How payments are formed

German tax return. Anlage WA-Est

Tax return in Germany. All income tax deduction

What is Girokonto in Germany

Girokonto is not in vain reminiscent of Giro d’Italia – the word is Italian and means “circle, circuit”. The money in this account is constantly spinning.

First of all, upon arrival, you will need it: for salary, for calculations with the landlord, for receiving child benefits, for paying for electricity, telephone / Internet / mobile …

Then there will be courses for children, taxes, kindergarten fees and everything.

Choosing a bank for the Girokonto is important because so many organizations use this account, and if you want to change it, you will have to remember and notify all these organizations.

Which bank to choose for Girokonto

Now the choice of Girokonto is not rich. Almost all of them are now paid. Although there was a period when we enjoyed free Giro even at the Volksbank.

Giro for young people under 26 and Giro for refugees can now be free. Theoretically, you can find a free Giro with a large monthly income, that is, if the salary is good. But such options are now rare, if at all.

There may also be free Girokontos in online banks, such as IngDiba (now just Ing).

For those who do not know German, the option of online banking is not very suitable: there you need to communicate in writing and with a telephone answering machine, and this is too difficult without a language. Therefore, most often the choice is narrowed down to local branches of Sparkasse, Volksbank or Deutsche Bank.

The first two are associations of a large number of local banks, so you can withdraw money in almost any hole in Germany, which is very convenient. However, their account conditions are different, you need to check every time and not think that if there are such conditions in Berlin, then so you also have.

Deutsche Bank emerges from the strongest crisis. A couple of years ago, I would by no means recommend opening an account there, but it seems that his business is getting better. In any case, accounts up to 100,000 euros are insured.

Another option, conditionally available locally, is Postbank. Some post offices have bank offices, and bureaucratic opening issues can be resolved simply at the post office.

If you like the conditions of an online bank or a less common bank (such as BMW Bank), be sure to check which ATM network you can withdraw money from for free and how common it is.

When choosing a bank, also note that some banks with filials have accounts that are cheaper because they are only serviced online.

What else to pay attention to

If you come with your family, then it matters what access to the account your partner has. If you trust her / him with finance, then she/he should also have normal access to the account. It can be one Girokonto for two, or simply extended access to the account, when the second person can carry out almost all operations with some restrictions.

The second important point is whether you want a credit card.

Credit cards linked to the account are usually very expensive (€30 per year). It is quite easy to find credit cards for 10 euros a year or even free ones with a good turnover on the card. More about credits in second part.

Thirdly, pay attention to the paper with the conditions that you are given when opening an account. There you will find information about which transactions are charged for what. For example, printing an invoice at a office might cost 50 cents, but copying the same online would be free. Withdrawing money from an ATM is free, but paying with a card every time in a store is 15-30 cents. You study what services are paid, and avoid them.

One example from life during a pandemic. All stores insisted on cashless payments. Fulfilling their wishes, I used the card. As a result, instead of 5 euros, servicing a Giro costed more than 10 euros per month.

For example

Kontoführung (Monatspreis) – account maintenance cost (per month)

Nutzung der Geldautomaten – ATM fees

Kontoauszüge an Kontoauszugsdrucker – fee for printing a report for month in a special printer in a bank (usually free of charge, if you didn’t have online-account). A printout of the bill must be taken regularly, otherwise it will be sent to your house (by law), but for this, most likely, they will charge a fee (appr. 1 euro)

Ein- und Auszahlungen – deposit/withdrawal fee

Beleghafte Buchungen – fee for transfers by paper or check.

Beleglose Buchungen – fee for transfers without paper (for example, via the Internet – but there may be a limit on the amount of online transfer per day (it can be changed if necessary)

Dauerauftrage einrichten, ändern – payment for permanent money transfers (for example, rent), for making or changing them

Maestro Card, Zweitkarte – a debit (not credit) card for withdrawing money from an ATM account and a second card for a second person

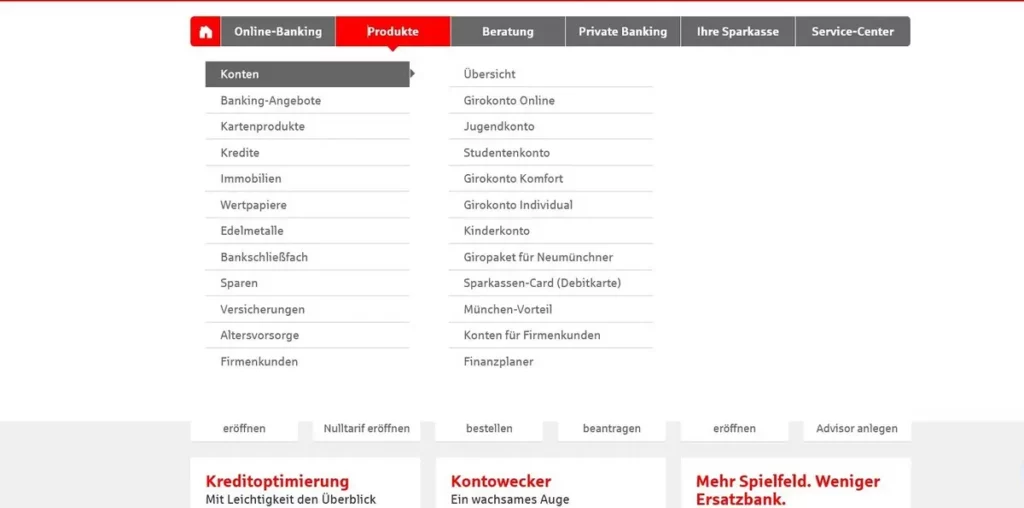

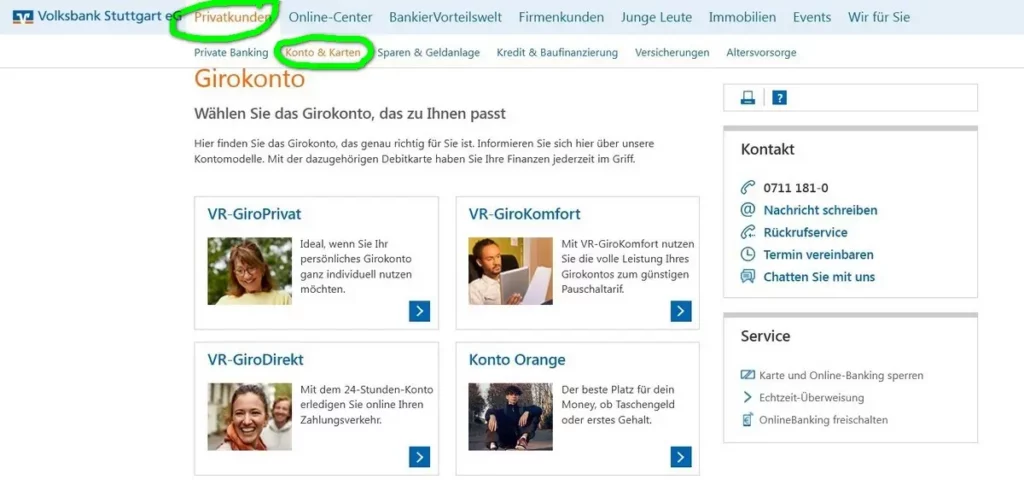

Let’s look at two Girokonto system – first is Sparkasse, second is Volksbank

To get to the giroconto we have to click on (Produkte or Private Kunde) – Konten – Girokonten.

We see some Girokonten. We don’t need Giro for Jugendliche or Stundenten. It should be Giro Online, Giro Komfort or Giro Individual by Sparkasse. By Volksbank: GiroPrivat, GiroKomfort or GiroDirekt.

Despite the different names, the meaning is the same – we pay less for an online account, more for a more individual approach with the ability to visit filials, and even more for a completely individual account.

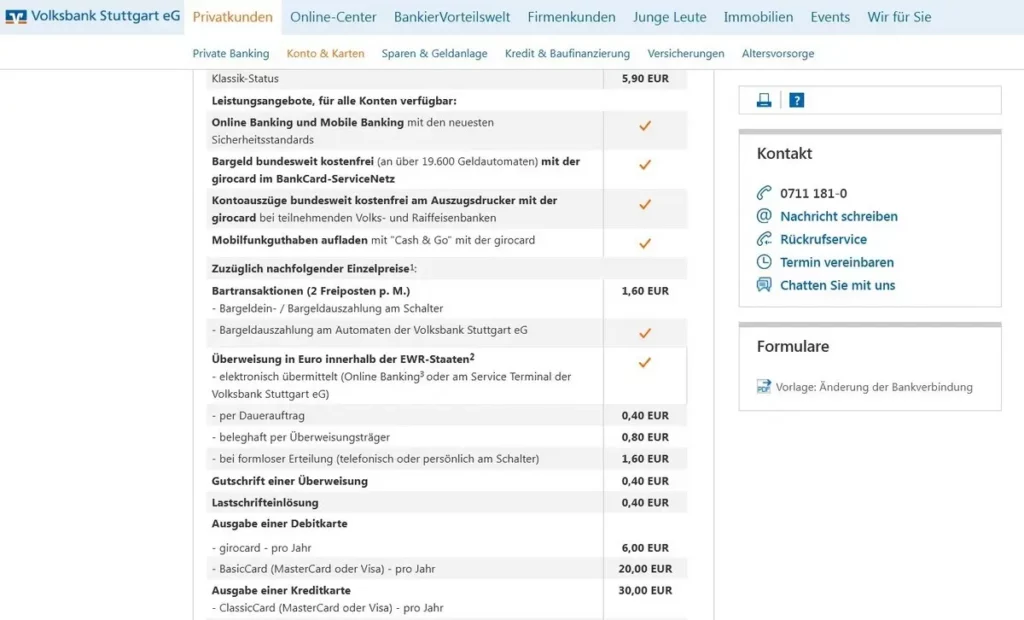

Prices (Konditionen) are the most important.

You see here, that for GiroPrivat by Volksbank you will pay 5.90 euro per month and also still for every permanent transfer (such as Kindergeld, or salary, or Miete) 0.40 euro.

Follow me

Do you have any more questions? Use comments ⇓ or private communication form ⇨

How to use Girokonto

So, you have chosen a bank and opened a Girokonto. You can be congratulated, but it’s too early to relax. Now we need to learn how to use it.

The main sin of the user of Girokonto is to go into the red!

This is heavily penalized by the banks (for example 9.90% by Volksbank). Since with the addition of leeches that suck money from your account, you no longer have so much control over when and who takes something from you, I recommend keeping a limit of 700-1000 euros on the Girokonto and not going below it to guarantee the maintenance of your account.

Best limit is in the amount of a month’s rent, then definitely no headache. If you have to go lower, then you must clearly track who and when you take how much per month. Imagine, for example, such a situation that you have less as rent amount on your account, and for some reason the salary was delayed and just this moment fell on the payment of rent.

Most modern girocontos have the ability to manage online. Don’t be afraid to use it. Yes, not all banks have a well-organized system, but when you orient yourself a little, it will be much more convenient than making every calculation through a filial.

Don’t forget to take your account statement regularly. Without online banking, it was necessary to print every month through a special machine. If we forgot to do this, they sent us a report by post and charged us an extra money (Gebühr) for it. In online banking, you can download statements in pdf format.

You need to look at statements. Occasionally there are unpleasant surprises. Our friends had their bank robbed, and my husband had money stolen from his credit card in Paris. In both cases, the money was returned, but such things need to be caught on time.

[shariff]Types of Girokonto transfers

Transfers can be one-time or permanent.

Permanent transfers- Dauerüberweisung (Dauerauftrag)

You can issue them yourself – through a bank filial office or through an online bank.

Or you can give permission to the organization that transfers or (more often) withdraws your money. This permission is called SEPA-Lastschrift. Don’t be afraid to sign this permission. You will get much more problems if you forget to transfer money to the organization, because you do not have a permanent transfer.

Already at the beginning of your stay in Germany, you must have permanent transfers:

- rent

- electricity fee

- (salary)

- (child benefits)

- Internet and mobile phones

- state television fees

- insurance Haftpflichtversicherung (insurance for damage that you or your children may cause to a third party, such as your landlord or loss of keys)

- (car insurance)

- (price for kindergarten)

- (public transport subscription)

By the way, about electricity. Sometimes it happens that a change of tenant passes by the electric company. A reader has already written to me about this. If you have not been sent anything about electricity and you do not know at all whether you are paying for it, this issue needs to be clarified urgently. Otherwise, you will have to pay later at once for all months in a very large amount.

Sometimes the organization does not want to make automatic transfers, but prefers to send you regular invoices for you to pay. Or you have a prepaid credit card. Or you regularly send money to someone. For example, I pay for meal to school every month.

In such cases, you can start a Vorlage in the online bank – that is, a sample. This can be done in the appropriate section or simply by clicking save as a sample (als Vorlage speichern) during the next translation. The next time you select this sample, you do not have to fill in all the data again, only change the amount.

Transfer (Überweisung) through a filial office

You will need a transfer through a filial office – not only if you do not use online banking, but also if you want to transfer an amount higher than the transfer limit in your online banking. For example, you will buy a car and pay 20000 euros. By the way, the limit can be changed.

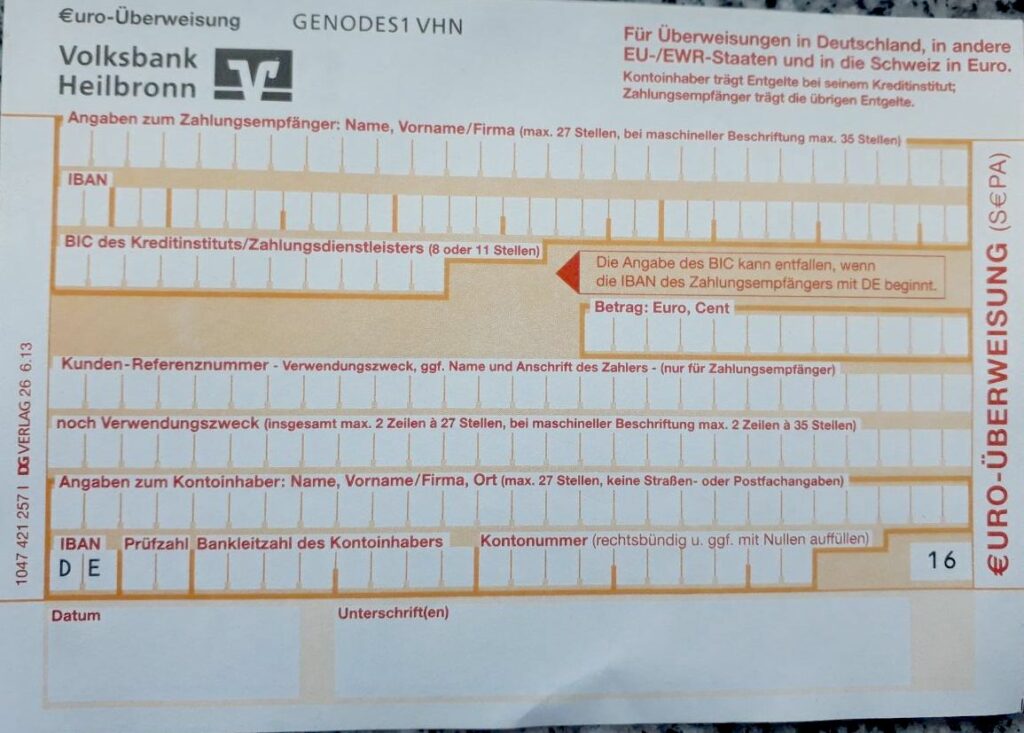

Consider how a transfer is made through a Überweisung formular. The formular is given to the a bank employee or sent to a special machine.

Let’s translate it.

At the top is the name of our bank and its BIC.

In the first line, we indicate the person who owns the account to which we transfer money.

Next comes IBAN – for German recipients, it starts with DE, followed by two specific control numbers, the bank identification number and your actual account number.

You can omit the recipient’s BIC if the recipient is in Germany.

Betrag – transfer amount. Cents are separated by commas.

Kunden-Referenznummer, Verwendungszweck – this is the number or those words by which your recipient can understand that the transfer is from you and for specific purposes. This is very useful even for ordinary users, and even more so for large organizations. As a rule, organizations write “als Verwendungszweck bitte Nummer….” on the invoice. This means that a certain number or name, words, must be indicated on the invoice in these lines.

Angaben zum Kontoinhaber – this is your name and your IBAN

Don’t forget the date and signature.

Transfer through online-banking

Transfer through online banking is similar to paper transfer. All the points that we discussed above are present there. BIC online is usually filled in automatically.

Next, you must prove that you are the one transferring the money, not the camel. Banks use different methods to do this.

Previously, it was a piece of paper with TAN codes. Most banks have now abandoned it.

The second option is a special TAN generator, a small machine where the card is inserted and which, in theory, should read the flashing code from the screen. By me theory never came true, and I had to manually fill in the necessary numbers (manuelle TAN-Verfahrung).

Finally, the most modern ones have switched to confirmation by mobile phone, with TAN sent by phone.

However, for transfers up to a certain amount, TAN is not required now (about 30 euros).

In the second part, we will consider what other accounts are in Germany.

All topics about #finance

Do you enjoy the site without cookies and maybe without ads? This means that I work for you at my own expense.

Perhaps you would like to support my work here.

Or Cookie settings change: round sign bottom left