Last Updated on September 27, 2023

In this post all tax deductions from E to H – from Education to Houskeeping Help.

Not forget: außergewöhnliche Belastungen (Exceptional costs) are deducted, if they over individual limit.

How to calculate the limit of außergewöhnliche Belastungen read here.

Other parts – A-D, I-N, P-W,

Other posts about german tax return – #steuererklaerung

Tax deductions in this post:

education

expenses over income

eyeglasses and contact lens

eye surgery

funeral

furniture

further education

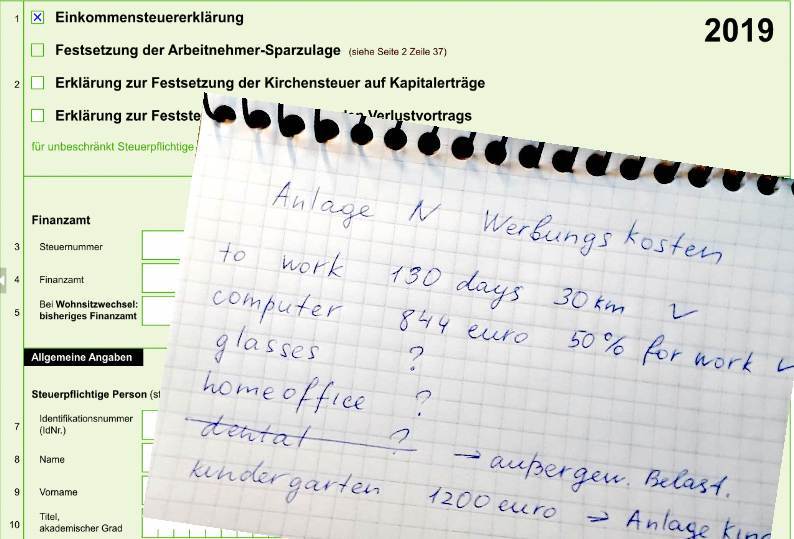

homeoffice

hospital

housekeeping help

Educatuion

The following are deducted as educational costs:

- interest on student loans

- cost of education (Semester-, Lehrgangs-, Prüfungs- und Zulassungsgebühren etc.)

- postage cost

- working materials (books, computer, office, desk)

- fare to the place of education

- cost of living (rent, Nebenkosten, Mehraufwendungen für Verpflegung (28 euros for a full day) etc.)

There is a difference in how these costs are taken into account. It depends on whether is this the first professional education or not, whether the student earns or not.

If the first education + the student does not earn, then, according to the rules, expenses are deducted as Sonderausgaben. This is up to 6 thousand per year).

If the first education + the student earns / or it is the second education, then the expenses go to Werbungskosten.

Werbungskosten in Anlage N

The first rule is considered dubious. A student can carry expenses to Sonderausgaben as much as he wants, but will receive nothing if he has no income. Therefore, it is recommended to record them in the Werbungskosten. I think that in this case it is better to turn to a tax consultant, since we are talking about large deductions, and the rules are not clearly defined.

If a student works part-time and has less income than expenses, or if he is getting a second education and does not earn now, but earned before, then he can apply for a Verlustabzug.

Part of the expenses can be deducted as a return from the previous tax return or postponed for other years when income appears.

Parents also have the option to deduct the costs of their child’s education.

For example, they pay the child’s rent and car insurance and the cost of gas. From this amount, 924 euros per year can be deducted as Ausbildungsfreibetrag. This applies to children who:

- are of age, are in education

- have right for Kindergeld

- do not live in the house

If children have right no longer for Kindergeld, these costs can be deducted as außergewöhnliche Belastungen.

Expenses over income

For expenses exceeding income, you can apply for a Verlustabzug. Losses can be deducted from taxes of the previous year or retained for the next year (or divided). For those students who suffer losses due to education, but did not have income before, there are difficulties with the deductions. So it is worth contacting a tax consultant.

Eyeglasses and contact lens

The cost of glasses can only be deducted as work expenses at Werbungskosten if

- the glasses are for computer use and nothing else

- and the person does not have other glasses to wear outside of work

- or if they protect their eyes by work.

In general, glasses and contact lenses are considered a medical device, not a work one. So their value can be deducted in the außergewöhnliche Belastungen.

Eye surgery

From the opinion that laser surgery to improve vision is a cosmetic surgery, the tax authorities are moving towards the opinion that this is the most common modern surgery that can be recognized for tax purposes in the außergewöhnliche Belastungen.

There are some different opinions in the sources, whether you need papers from an ordinary ophthalmologist or Amtsarzt. It is possible that this varies from Bundesland to Bundesland. Before deciding on an operation, ask what papers you need to collect.

Funeral

This is the point that everyone chooses not to think about, but life is unpredictable. Therefore, you need to know that funeral expenses can be deducted in the außergewöhnliche Belastungen only if they exceed the inherited inheritance. Inheritance includes not only money, but also insurance, real estate, jewelry, as well as moneyfrom insurance if death was due to someone else’s fault, and compensation from the employer.

In this case expenses can be deducted in amount, which is over as the inheritance.

Furniture

Furniture can only be deducted in three cases:

- when it is the minimum necessary furniture for the second apartment for work needs (doppelte Haushaltsführung)

- it is office furniture or furniture for work’s room

- it is a furiture for renting furnished apartment

In any of these cases, furniture is written off within one year if it costs up to 800 euros netto (before 2018 – up to 410 euros), and within several years if it costs more. See “working costs” for details.

Werbungskosten in Anlage N. “Work’s” cost in All I can return – part P-W

Further education

Courses that give you the opportunity to improve your work skills in your profession (Fortbildung) or transfer to another profession (Weiterbildung) can be counted as Werbungskosten if your employer has not compensate you. Courses can be held all day long, or part of it, or in the evening after work.

Deducted expenses include:

- cost of courses and exams

- travel to the place of training. If these are full-day courses for several days, then travel is counted once

- hotel accommodation cost

- the cost of food as Verpflegungskosten. There is a list – it depends on the number of hours. For example, a business trip for several days – 28 euros per day (from 2021, before – 24 euros). Days of arrival and departure at a separate rate.

- the cost of training materials (books, office supplies)

Werbungskosten in Anlage N

Homeoffice

In 2020-2021, a home office pauschal was introduced (5 euros per day, but not more than 600 euros per year).

More about Home office in another topic. What else is changing in 2021 – read here.

Hospital

Travel and hospital costs are deducted as außergewöhnliche Belastungen if they have not been compensate by the Krankenkasse. Inpatient treatment must be prescribed by a doctor.

Housekeeping help

Many domestic helpers or caregivers work unofficial. This is cheaper for the employer and makes less of a problem with papiers. But unofficial workers are regularly caught, which threatens the employer with very heavy fines and even imprisonment. In addition, any accident on your territory can make trouble.

Officially helpers have to conclude an agreement with you. And you become then a real employer with all social obligations. Or you register him as a “mini-job” through Minijob-Zentrale, if the amount you pay him a month is less than 450 euros.

Follow me

You can deduct 20 percent of the assistant’s salary from taxes. But in the case of a mini-job, this amount is limited to 510 euros per year. And in the case of a full-time employee – 4000 euros per year. Money must be transferred to accounts.

The money is written off through the lines of Haushaltsnahe Dienstleistungen. Until 2019 it was in Mantelbogen, from 2019 – in a separate Anlage.

Anlage Haushalthahe Aufwendungen.

Expenses are also written off there if you hire an employee through a company for household works. In this case, the limit will be 1200 euros per year. This can be a janitor, cleaning lady, glass washer, carpet cleaning at home, cook, ironing, repair, gardener, snow cleaning, caring for the elderly and sick, nanny, caring for animals on your territory (supervision in your absence, haircut), moving costs (in terms of labor costs), chimney sweep.

A worker can be hired by your landlord or condominium. In this case, the cost of the work is included in the Nebenkosten, about which you receive the corresponding paper. The amount that can be deducted must be indicated in the invoice separately. The money has been transferred to the account, and not in cash.

Can be deducted:

- labor costs (Arbeitskosten ohne Mehrwertsteuer),

- travel expenses,

- equipment operating costs,

- consumables (such as snow salt or detergents).

Can not be deducted:

- the cost of materials (for example, a new lock that was supplied to you),

- expenses for a management company in condominiums,

- garbage collection and delivery costs.

All I can return from tax: A-D, E-H, I-N, P-W

Anlage N Part 1, Part 2, Anlage N-Aus, Anlage Wa-Est, Homeoffice

Anlage Kind

Anlage Vorsorgeaufwand

Anlage Sonderausgaben

Anlage Haushaltnahe Diensleistungen 35a

Who should file a tax return in Germany

Pre-filled declaration in Elster

How to calculate tax in Germany. What is written in Berechnung in Elster

Freiberufler in Germany: how to fill in Anlage S and Fragebogen zur steuerlichen Erfassung

Do you enjoy the site without cookies and maybe without ads? This means that I work for you at my own expense.

Perhaps you would like to support my work here.

Or Cookie settings change: round sign bottom left