Last Updated on July 12, 2024

Anlage N-Aus is definitely not simply, also if you are not sure, it is better to go to the tax consultants for the first time (in LohnsteuerHilfe Verein). But it is possible, that you don’t need this application at all. Anlage N-Aus – for those who already live in Germany and make some work abroad.

If you are first year in Germany or leave it this year, then you need Anlage WA-Est. it has existed since 2017.

Read about Anlage WA-Est here.

All I can return from tax: A-D, E-H, I-N, P-W

Anlage N Part 1, Part 2, Anlage N-Aus, Anlage Wa-Est, Homeoffice

Anlage Kind

Anlage Vorsorgeaufwand

Anlage Sonderausgaben

Anlage Haushaltnahe Diensleistungen 35a

Who should file a tax return in Germany

Pre-filled declaration in Elster

How to calculate tax in Germany. What is written in Berechnung in Elster

Freiberufler in Germany: how to fill in Anlage S and Fragebogen zur steuerlichen Erfassung

Is interest income taxable in Germany? Bank bonuses and interest income in declaration

I remind you that I translate and collect information that I can find, but I am not a tax consultant.

I have still more questions, and I’m not sure in answers. There is no normal review of the application on the network, basically all reviews with the same words, as in Elster’s help. And there was not even an interview mode for this application in it.

To fill out the application with confidence, you need to read the double taxation agreements, know what is taxed and not taxed, and have a good knowledge of Werbungskosten.

Do not forget about the deduction of the move and double households.

Read about Werbungskosten in topic All I can return, part 4

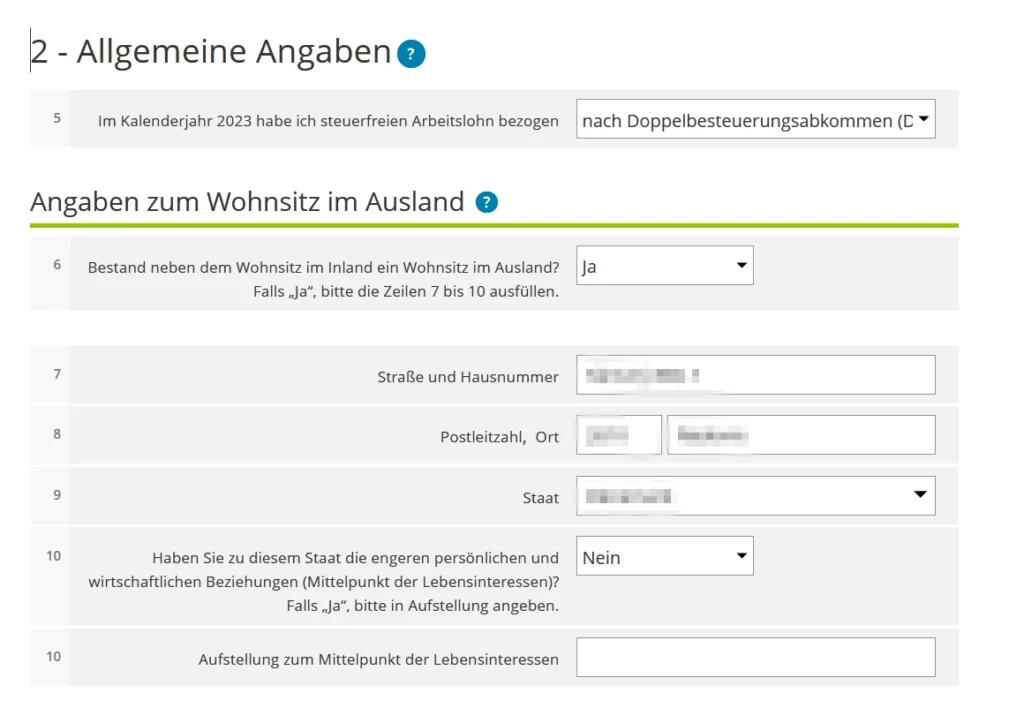

General information in Anlage N-Aus

Line 4 – select the country where you worked.

Line 5 – Taxation under DBA double taxation agreements or special agreements (second line). What countries have such agreement – look at : link.

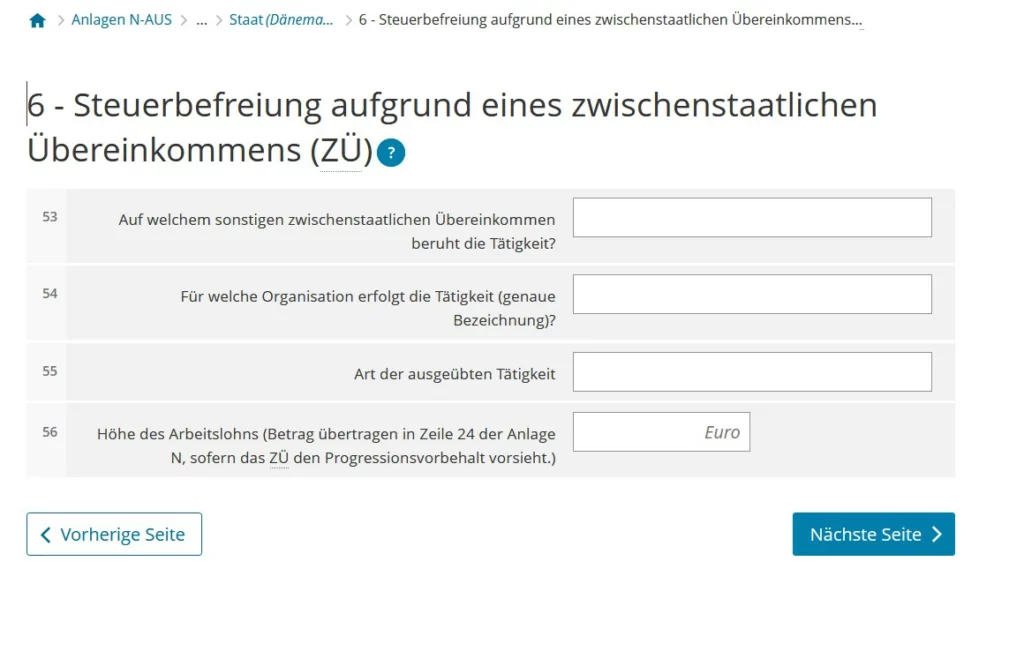

Special agreements ZÜ, if I understand correctly, these are all sorts of international organizations (list here), such as NATO troops, the UN, etc.

ATE – those who do not fall under the double taxation agreements, i.e. no such agreement has been concluded with the country.

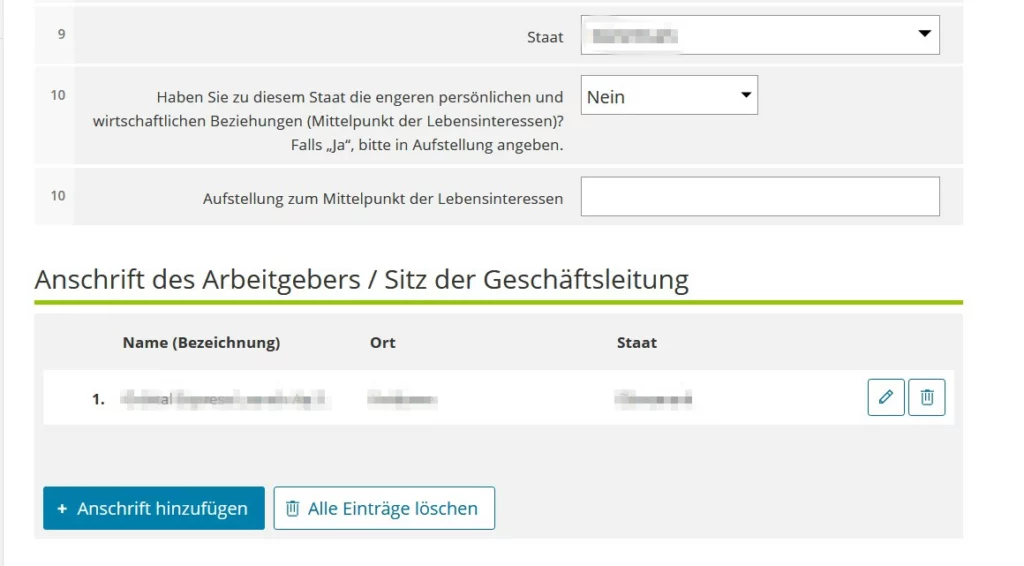

Line 6 – do you have housing at a foreign country, where you worked, or not.

Lines 7-9 – address.

Line 10 – do you have interests in that country (for example, you have a wife and children there) and what interests.

Line 11 – employer information.

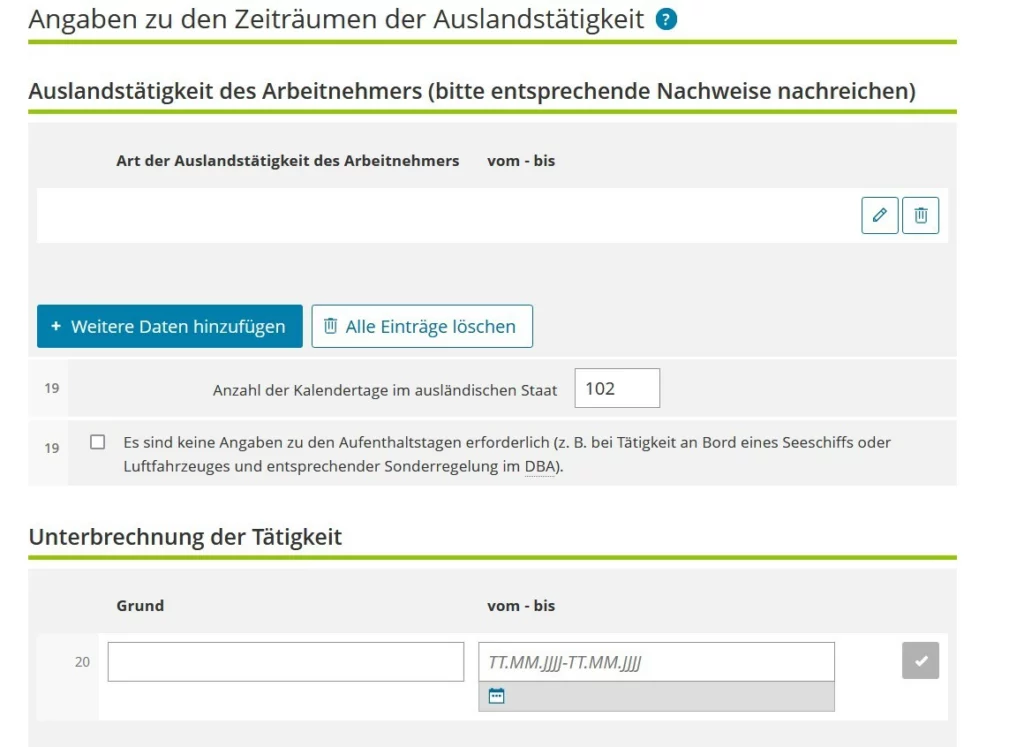

Lines 19, 20 – what exactly did you do and in what period (how many days, including weekends)

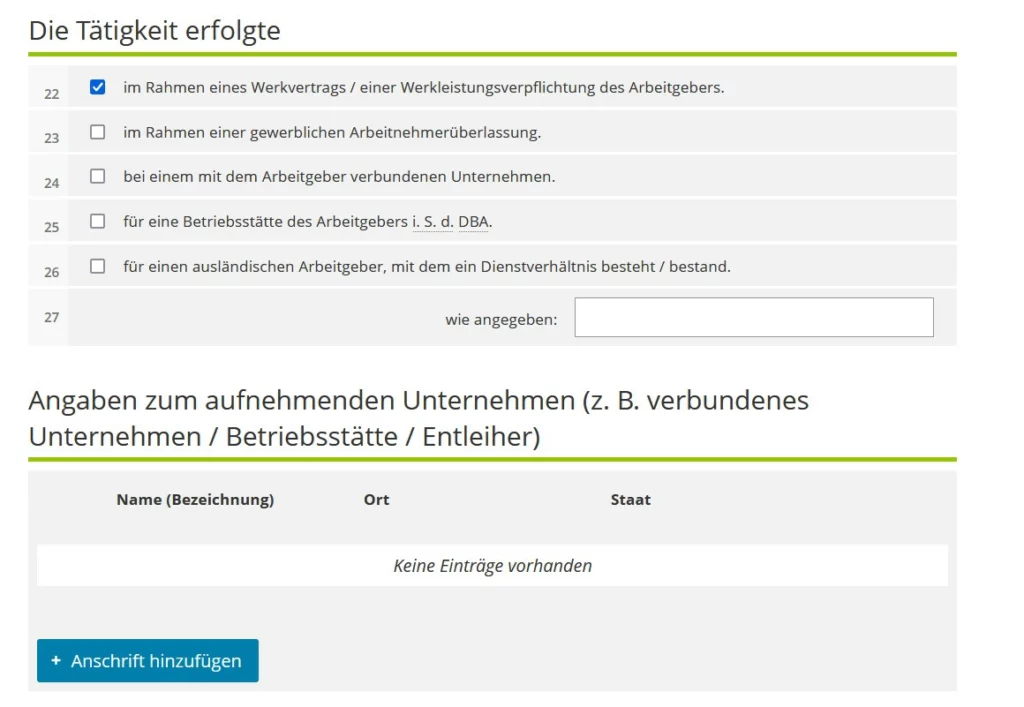

Line 22 – under an employment contract with an employer.

Line 23 – for outsourcing.

Line 24 – in the company associated with the employer.

Line 25 – in the foreign branch of the employer (if the period exceeds 183 days).

Line 26 – if services were provided.

Line 28 appear to be for the host organization if you did not work for your employer but for a related company or branch.

Income

Enter gross income in lines 32-33. In this case, gross should be calculated according to German laws, and foreign currency should be converted into euros at the average monthly rate of the European Central Bank (link according years).

That is, the salary for each month should be transferred, then summed up.

On line 32 the amount for German income, on line 33 foreign income.

Line 34 – tax-exempt income on lines 16 of the German tax calculation (if any).

Line 36 -im Ausland steuerpflichtiges, in Deutschland jedoch nicht steuerpflichtiges Einkommen

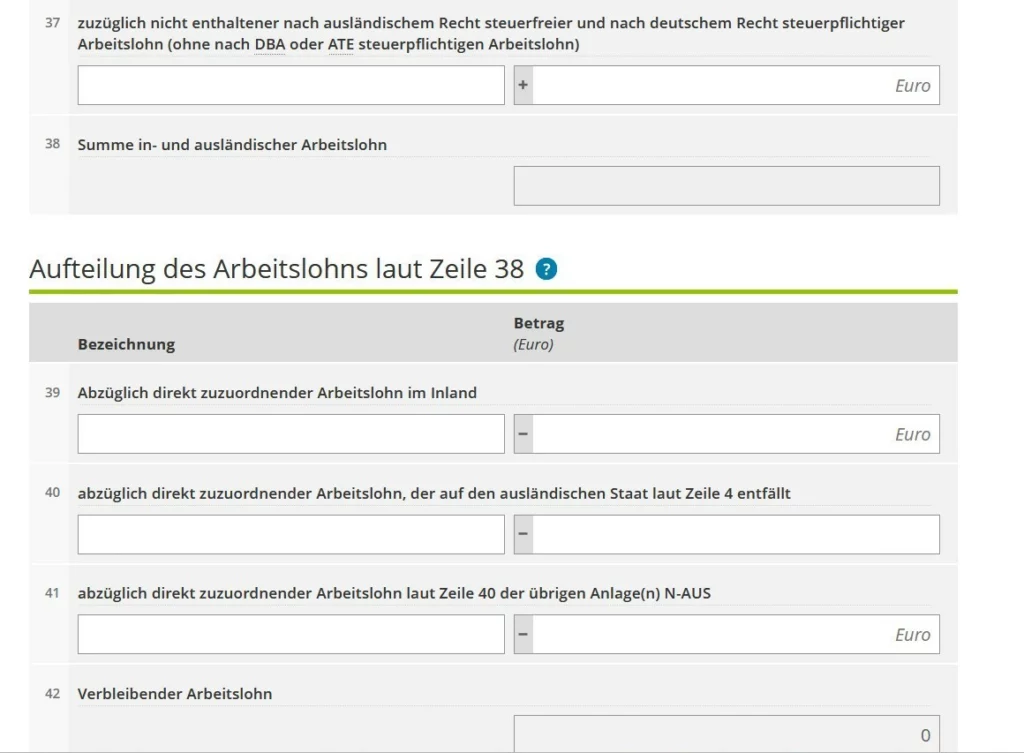

Line 37 – income not taxed abroad but taxed in Germany (without salary)

Further, for me the most incomprehensible lines. On one forum a typical situation was discussed: part of the year in one country – income is taxed, part of the year in Germany – income is taxed. I resume what people think about it.

Line 39 is the taxable salary in Germany. This also includes all income directly related to work activities: additional payments for additional work, work on weekends, etc.

Line 40 is the salary abroad, it was taxed there and it relates directly to work activities.

Line 41 – other overseas salaries, they were taxed already – if there are any on other Anlage N-Aus.

The balance may remain amounts that are not directly related to work in the certain country. They must be distributed mechanically according to the number of days worked there and there. Which is what is done in the following lines.

Line 43 – the number of real office days: the amount abroad and in Germany, to that line 44 – abroad.

Line 45 – the percentage related to foreign work is calculated from those incomes that could not be clearly attributed to a particular country if they were indicated in line 42.

Follow me

If the balance on line 42 is zero, then all remains as it is:

- German income will be taxed according to German laws,

- foreign income will not be, since it is already taxed,

- but their amount will go to Anlage N and increase the grade (Stufe) for taxation.

And in order not to get a significant progression, you need to indicate your operating costs (Werbungskosten) in lines 57-59.

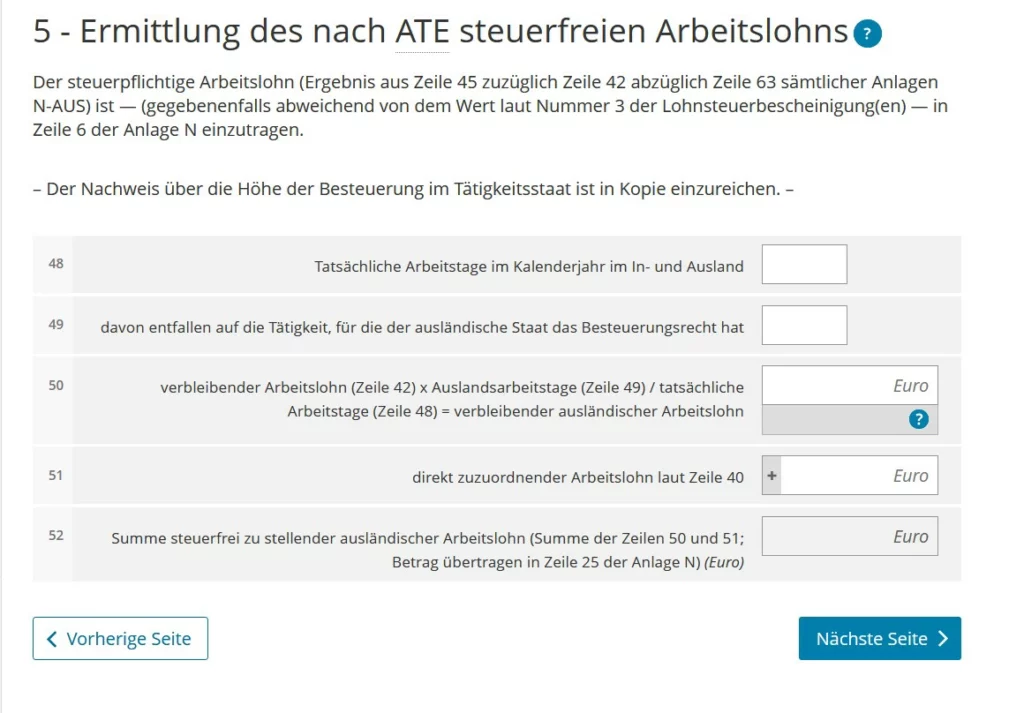

Lines 48-56 for ZÜ and ATE.

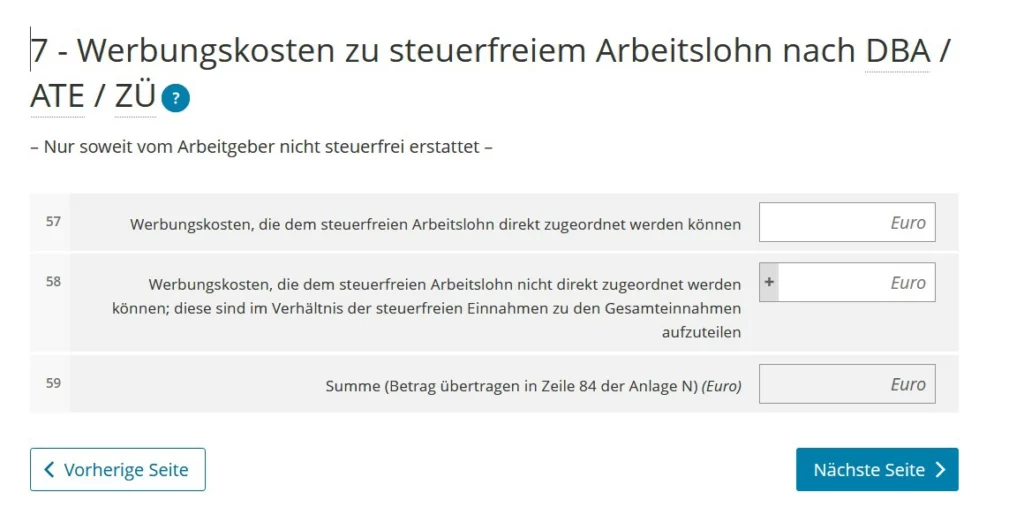

Lines 57, 58 for Werbungskosten

Line 57 – expenses directly related to work, for example, travel to work.

Line 58 – other expenses (for example, office or labor) in terms of income not taxed in Germany. That is, if you bought working tools that will be useful to you in Germany too, then you should only take into account the value attributable to the part of income abroad (for example, 30 percent).

Insurance does not apply to work expenses, only legal assistance on work conflicts. The forums offer to record insurance abroad in Sonderausgaben. However, regarding pension insurance, they write that it is impossible to deduct those insurances that relate to activities exempt from taxation in Germany. That is, pension insurance for work with a foreign employer is not suitable when it is exempt from taxes under the DBA agreement.

For the Werbungskosten, it is recommended that you include an explanation of which costs you wish to deduct.

About Anlage Sonderausgaben.

About Werbungkosten – All I can return. Part 4

Other posts about German tax return – #steuererklaerung

All I can return from tax: A-D, E-H, I-N, P-W

Anlage N Part 1, Part 2, Anlage N-Aus, Anlage Wa-Est, Homeoffice

Anlage Kind

Anlage Vorsorgeaufwand

Anlage Sonderausgaben

Anlage Haushaltnahe Diensleistungen 35a

Who should file a tax return in Germany

Pre-filled declaration in Elster

How to calculate tax in Germany. What is written in Berechnung in Elster

Freiberufler in Germany: how to fill in Anlage S and Fragebogen zur steuerlichen Erfassung

Is interest income taxable in Germany? Bank bonuses and interest income in declaration

Do you enjoy the site without cookies and maybe without ads? This means that I work for you at my own expense.

Perhaps you would like to support my work here.

Or Cookie settings change: round sign bottom left