Last Updated on May 1, 2024

After a fairly long period of interest rate drought, the banking situation has returned to more normal. Interest income began to flow into savings accounts again, and banks began to lure clients with bonuses. What does Finanzamt think about this? In this topic, we will consider when and how to document interest income and bonuses in the German tax declaration.

Deductible expenses for second home for work in German tax return

What is Riester pension

Pre-filled declaration in Elster

How to calculate tax in Germany. What is written in Berechnung in Elster

Who should file a tax return in Germany

Tax declaration Germany. Anlage EÜR

German income tax declaration. Anlage N-Aus

German tax return. Anlage WA-Est

German income tax declaration. Anlage Vorsorgeaufwand

German tax return Elster. Anlage Sonderausgaben

Elster online. 6. Household works deduction – Anlage Haushaltsnahe Aufwendungen (35a)

Tax return in Germany. All income tax deduction P-W

German tax refund – What I can claim to return. I-N

I am not a tax consultant and I am not responsible for the contents of your tax declaration.

Although you receive both bonuses and interest from the bank, the situations are different and have different tax consequences. Interest on deposits is income from investment (Kapitalertrag), and the bonus is irregular income not related to work. Let’s start with interest.

Is interest income taxable in Germany

Let’s start with the fact that up to a certain amount, interest income is not taxed at all. This amount, called Sparerpauschbetrag, has long been 801 euros per person (1,602 euros for spouses). From 2023 it is 1,000 euros per person (2,000 euros for spouses). Sparerpauschbetrag applies to interest on deposits, dividends, income from the sale of stocks and similar transactions (Termingeschäfte).

However, the bank initially does not know that the few euros of interest that have accumulated on your account are all your interest income. It considers you an infinitely wealthy person and therefore withdraws interest income tax. At the end of the year you receive a report that you have been taxed.

The German income tax is not small: 25 percent of the tax itself, which is called Abgeltungssteuer, plus 5.5 percent Soli (the tax for the eastern federal states, which is still in force for high earners and excess income). The churchgoers will also have to share with the church.

Abgeltungssteuer is withdrawn automatically from interest on accounts and depots in German banks, unless you have exempted part of the income from tax.

So, if the bank writes to you at the end of the year that your interest amounted to this much and tax was taken from it, you can leave everything as it is and not report anything in the declaration. Your duties to the state have been fulfilled.

If this money was overpaid because you were not aware of the tax exemption or forgot to fill out the form, then it can be returned. We’ll find out how to return it a little later, but for now let’s see how to be exempt from tax.

What is Freistellungsauftrag

To exempt yourself from taxation in advance, at all banks where your deposits are kept, you fill out a special form – Freistellungsauftrag. You determine the exemption amount yourself, the main thing is that the amount of all exemptions in all banks does not exceed 1000 (2000 for spouses) euros.

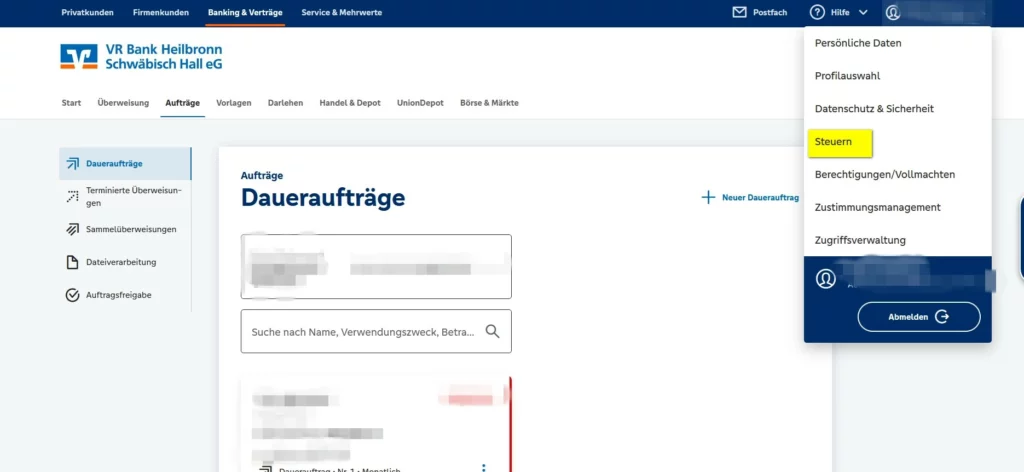

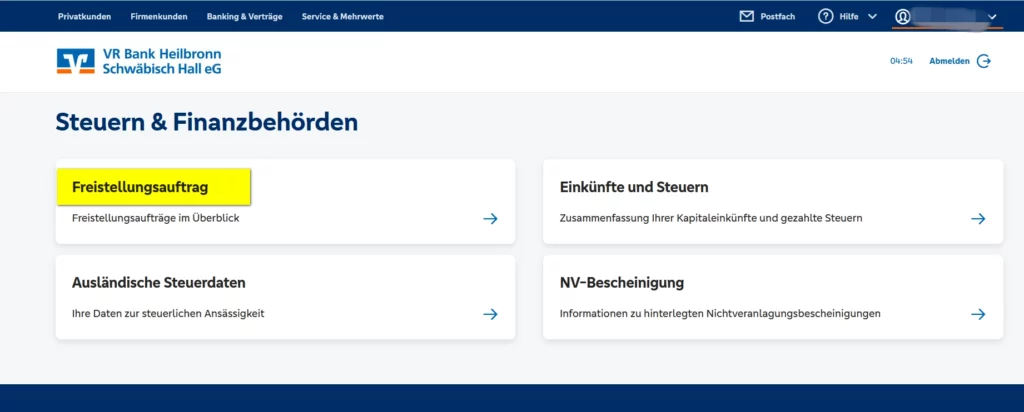

You can find the application form in your online banking (can be filled out online and validated in the same way as a transfer) or ask for one at a filiale.

For example, at the Volksbank this form is located in the Steuern section:

Fill out Anlage Kap

Now let’s return to the question of when and how to report interest income in the German tax declaration.

You need to report interest income in your German tax return in the following cases:

- if you received interest from a foreign bank

- if you have an investment deposit in a foreign bank

- your bank did not take into account everything that was needed, for example, it did not take into account some losses or did not charge you church tax, although you must pay it

- if you lent money to a private person at interest

- if Finanzamt owes you payments and gives them to you with interest

- if you want to return overpaid interest income tax

- If your entire income is small – more than the taxable minimum, but taxed at a rate of less than 25 percent – you can apply your rate for other income to interest income tax.

- if your interest on deposits or dividends are high and tax has been taken from them, but your entire income is less than the taxable minimum, then your income should not be taxed. In this case, you can also return the already paid interest income tax.

This can apply, for example, to children or students who already have large accounts of their own, or pensioners with a small pension but large savings. To avoid having to fill out a declaration and return the tax every time, you can apply for Nichtveranlagungsbescheinigung at the Finanzamt.

Interest income is entered into the Anlage KAP application. It has two additions: Anlage KAP-INV and Anlage KAP-BET. The first addition is for those who have their investments in foreign funds or banks, the second is for those who have a share in a partnership.

Each spouse fills out their own Anlage KAP application, which, however, is also true for many other applications. But, a little difficulty awaits us here. Often spouses have joint accounts, and if both spouses reports the entire amount into their Anlage KAP applications, then the return will be double. Therefore, if the account is joint, the amounts relating to it are divided. For example, a family has received 80 euros interest income from joint account. Each spouse reports in own Anlage KAP 40 euros.

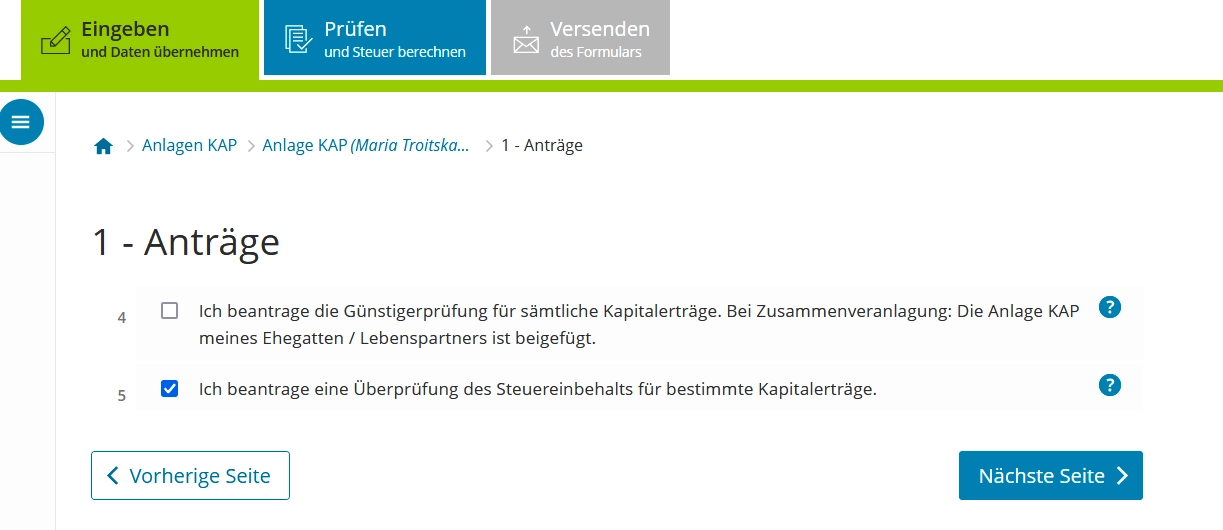

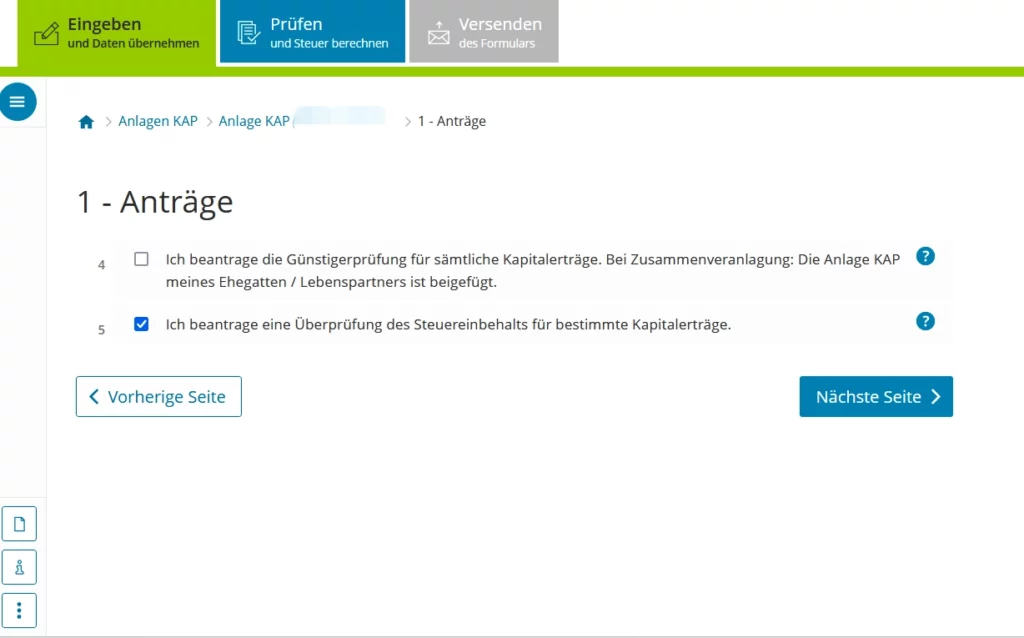

Let’s look at the Anlage KAP application, not in detail, but only those lines that relate to simple cases, for example, overpaid interest income tax. We will leave investments and participation in partnerships to tax consultants.

Line 4 for those whose entire income is taxed at a rate of less than 25 percent. By checking this box, you are asking the Financial Officer to recalculate the interest income tax in accordance with the rate on other income. If you are wrong and your rate is above 25 percent, you will not be charged any extra tax. In this case, you will not lose anything.

Further you indicate the amounts of all interest income received, including those that were exempt from taxation.

Line 5 – you check the box if you paid too much:

– because you incorrectly distributed (forgot about) the tax exemption

– or because the bank did not deduct your losses from your profits on dividends/shares

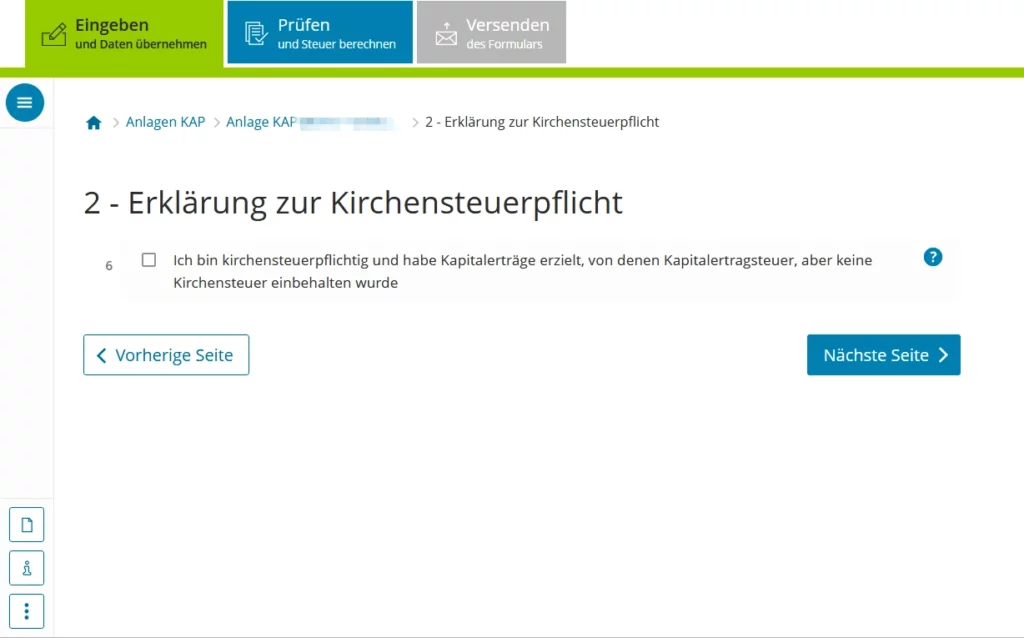

Line 6 is for those from whom the bank forgot to collect church tax. In this case, only those amounts that need to be additionally taxed with church tax appear in the following lines. That is, if one bank did everything correctly, then these amounts do not need to be indicated, but only the amounts received in another, “forgetful” bank.

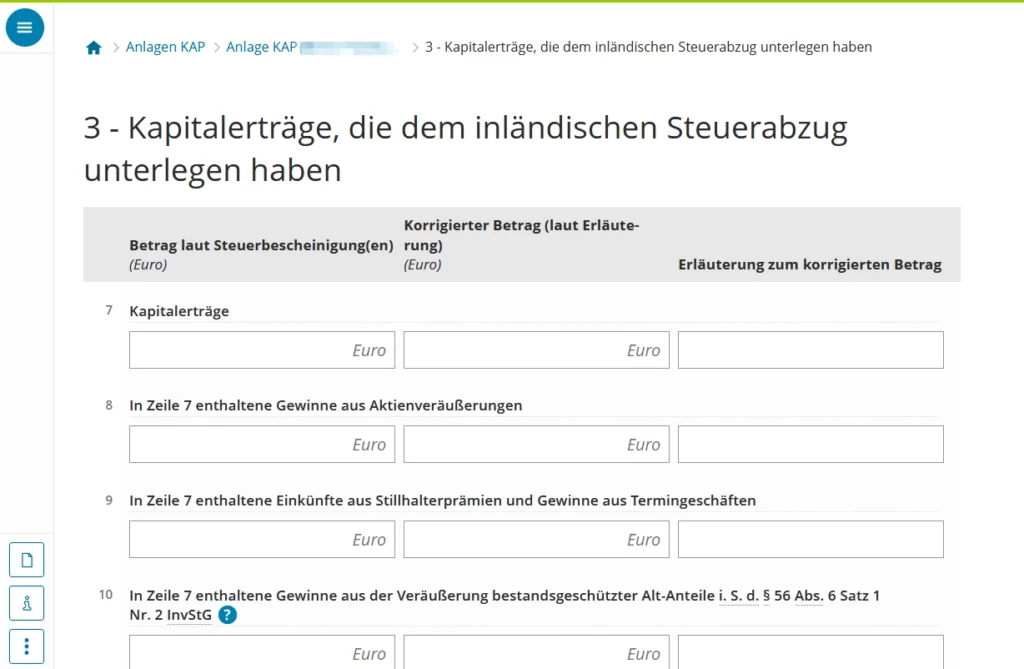

Line 7: Enter your interest income, from which you have paid tax. If you have multiple sources, summarize them. The second column is for those who want to adjust the taxable amounts, for example, if the bank did not take into account losses.

For those who want to return what they overpaid (line 5 is marked). If some of these sources were not taxed because they did not exceed the amount specified in the exemption Freistellungsauftrag, then you do not report this income here.

For example, you received 600 euros of interest in one bank and 80 euros in another, but in the first bank you filled out an exemption for 800 euros, and in the second you forgot. You indicate only 80 euros on line 7, and 600 euros will be indicated further on line 17.

For those who want to pay extra church tax (line 6 marked). Indicate only those incomes from which you must pay extra.

For those who want to change the rate to a lower one (line 4 is marked). Indicate all interest income.

Lines 8 – 15 cover gains and losses from stocks and other similar investments. As already mentioned, I will not delve into this difficult area as uninitiated person. If it is possible to invest money in this way, it makes sense to set aside some money for a tax consultant.

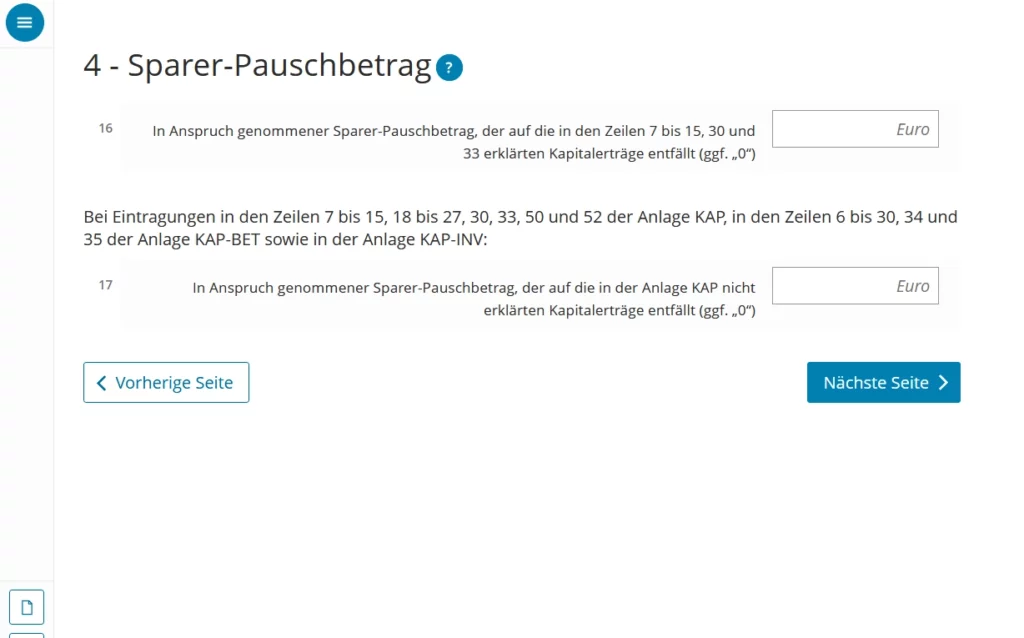

Line 16 is the amount of the Sparerpauschbetrag exemption that was applied to the amounts indicated in lines 7-15, as well as further in lines 30 and 33. Here you indicate the amount that was deducted before taking the tax.

For example, you received 1000 and 500 euros of interest in two banks, the exemption was in one bank for 800 euros, and in the other for 300 euros. Accordingly, in line 16 you indicate 1100 euros.

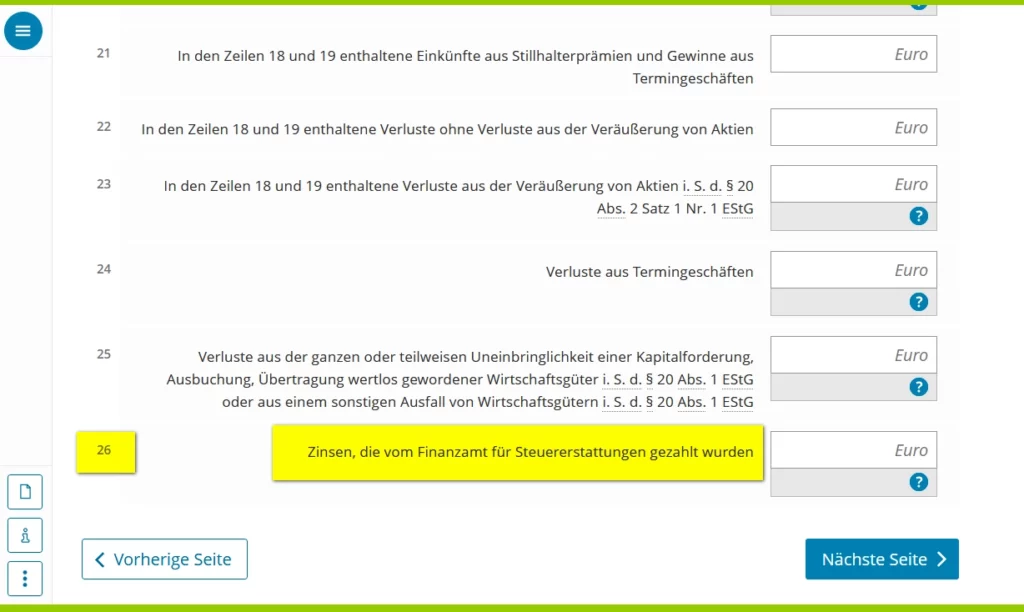

On line 17, you enter the amount that was not taxed because it is less than the tax exemption amount you requested from that bank and that was not mentioned in line 7.

That is, if the bank has exemption for 600 euros, you received 505 euros of interest, then you indicate 505 euros in this line.

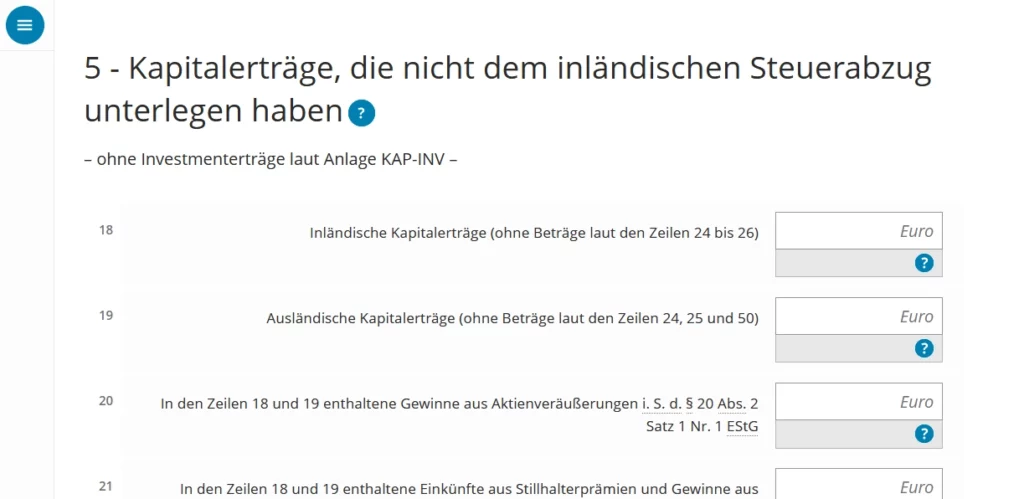

The next page is about interest income that was not taxed in Germany. It can be:

– the amount of interest you received by lending money as an individual.

– or interest from foreign banks.

Line 26 shows the interest paid to you by the Finanzamt. This happens rather rarely, since Finanzamt gives itself a fairly long period for returns and it usually doesn’t come down to interest.

Lines 27 to 30 are investment income, which is subject to your tax rate and not to the 25 percent interest income tax. These are rarely seen types of income.

Here we will pay attention only to line 30 – interest income from Lebensversicherung with capital.

More about Lebensversicherung (life insurance)

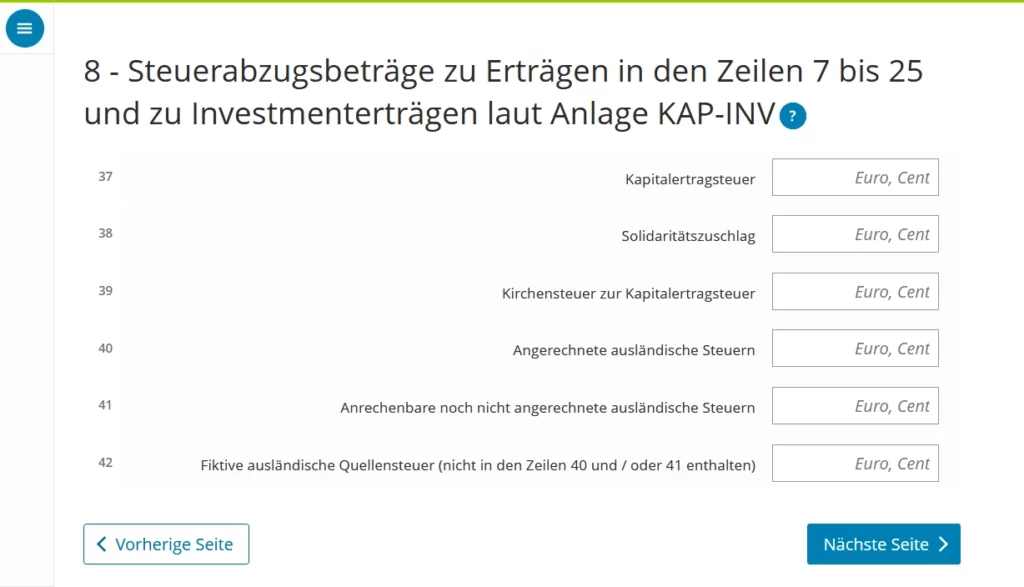

We skip the next lines until section 8. Here we must indicate how we were taxed.

You take this data from your bank’s report. If the bank did not send the report and it is not in your online banking mailbox either (which is rather unlikely), you need to request this report at the bank.

Line 37 – how much tax was withdrawn from you in relation to the amounts that you indicated in lines 7-25. Let’s not forget that the spouses divide both the interest and the tax that was taken from them into two Anlage KAP applications.

Line 38 – paid Soli

Line 39 – paid church tax

Next are foreign taxes if your source is overseas. The following pages do not apply to us.

Reporting of a bank bonus for a new client in Anlage SO

Bonuses are a nice thing, but you should control amount so that you don’t unexpectedly get taxed on them. The bonus received from the bank is considered income and is included in the declaration in Anlage SO.

Anlage SO – this is such a hodgepodge of various incomes not related to work: alimony, income from the sale of real estate, etc.

This category of income remains tax-free up to 256 euros. If your income in this category is higher, the entire amount is taxed.

Bonuses go to line 8. If there are any expenses associated with receiving a bonus (for example you have to drive to the bank), then they go to line 11, the result – to line 12.

And now the question is: what to do with bonuses from the electric company and other similar ones? While the opinion regarding banks and depots is clear, I can not find opinions regarding bonuses from electric companies.

The only information I found: the court believes that if such a bonus was paid directly into the bank account (Sofortbonus), then it is income and should be reported as income for calculating unemployment benefits. If you didn’t receive this money in your hands, then this is not income, and the discount does not count.

Deductible expenses for second home for work in German tax return

Pre-filled declaration in Elster

How to calculate tax in Germany. What is written in Berechnung in Elster

Who should file a tax return in Germany

Tax declaration Germany. Anlage EÜR

German income tax declaration. Anlage N-Aus, Anlage WA-Est

German income tax declaration. Anlage Vorsorgeaufwand

German tax return Elster. Anlage Sonderausgaben

Elster online. 6. Household works deduction – Anlage Haushaltsnahe Aufwendungen (35a)

Tax return in Germany. All income tax deduction P-W

German tax refund – What I can claim to return. I-N

All tax deductions (in German income tax declaration). E-H

All income tax deduction (in German tax return). A-D

Do you enjoy the site without cookies and maybe without ads? This means that I work for you at my own expense.

Perhaps you would like to support my work here.

Or Cookie settings change: round sign bottom left