Last Updated on January 30, 2024

Are you renting (buying) a second home to spend the night closer to work? This will be called Doppelte Haushaltsführung. There are a number of deductible expenses for second home in Gerrman tax return. Let’s take a closer look at how this is done using the example of an employee. An individual Self-employed can also rent a second home (and write them off as Betriebsausgaben). The principles of deduction will be the same.

It also makes sense to review the rules and restrictions for those who are just thinking about whether or not to take such a job that you will have to rent a second home.

Who should file a tax return in Germany

Home office tax deduction in german tax return

Elster online. 6. Household works deduction – Anlage Haushaltsnahe Aufwendungen (35a)

Tax return in Germany. All income tax deduction P-W

German tax refund – What I can claim to return. I-N

Tax return in Germany. Elster online. Anlage N. Working expenses

Pre-filled declaration in Elster

German income tax declaration. Anlage N-Aus

Tax declaration Germany. Anlage EÜR

How to calculate tax in Germany. What is written in Berechnung in Elster

I am not a tax consultant, do not provide tax advice, and am not responsible for the contents of your tax return.

Before we move on to deductions, an answer to the question for those who are thinking about whether to take a job far away, whether the money spent will be returned and by how much they should demand a salary increase.

The monthly deductable limit is 1000 euros net, almost 1200 euros gross. Plus trips home, home office, if there was one, trips from the second home to work. Plus up to 5,000 for the purchase of things for the home (according to the list limited by the tax authorities). All this together will not be returned to you in pure sum, but will be deducted from the tax and will lower the tax base, and with it the tax level.

Let’s say your salary is 95,000 euros, you were able to confirm 12 thousand expenses for second home, which means the base has been reduced to 83,000 euros. From this base, the remaining Werbungskosten (say 400 euros) and social contributions (say 11,000 euros) are also deducted. The tax in this case will be 13,540 euros and will be further reduced by the cost of Nebenkosten. If there were no 12,000 euros of recognized expenses for the second home, then the tax would be 17,600 euros. Thus, out of 12,000 euros of recognized expenses, you will return about 4,000 euros, that is, a third. Anything that does not fit within the limit of recognized expenses (and this can happen with housing if you do not find it less than a thousand net) will remain hanging on your wallet. Of course, this calculation is approximate and rounded. Take your own tax return from the previous year and put in Werbungskosten your estimated expenses for a second home.

How to understand Berechnung from tax office and how to calculate tax: How to calculate tax in Germany. What is written in Berechnung in Elster

Now let’s move on to deduction of expenses for a second home.

When can you deduct expenses for a second home?

Requirements for a second home

It is important that the second home is needed specifically for work purposes, and this is the main place of work. If you work in one place and periodically go somewhere overnight, then this will be processed differently.

You can get a second home for work purposes if it takes you more than an hour to get to work and the second home saves you at least half of your travel time.

The tax office is well aware that getting a second home very close to work is not always possible. However, distances greater than 50 km still seem dubious to her. In this case, you will have to prove that you are saving time and traveling no more than an hour to work.

So, you work during the week, for example, in Berlin, and on weekends and holidays you are at home in Cologne. Previously, in such cases, people often rented a room or apartment. Now, with the development of home office, the “three days at work, 2 days home office” or “three weeks at work, one week home office” and similar models have become popular. It has become cheaper to rent a hotel these days than to pay rent. There is no deposite, no obligatory Kündigungsfrist, you do not pay rent while on vacation. Of course, there are also negative aspects: if in the large city where you work there are large exhibitions or some kind of Oktoberfest, then within a month you will not find any hotel or you will find it for such money that it will fit into the monthly budget.

The question arises: are such changing hotels also a second home? On some sites, which in my opinion are not reliable enough, the same phrase is repeated that changing hotels are an overnight stay “gelegentlich” and it is supposedly written off differently. But, firstly, no one knows how it is different, and secondly, on other sites, which are much more convincing, they say that there is no difference with an apartment or a permanent hotel.

In our case, changing hotels were accepted.

Thus, second housing can be:

– rented apartment

– rented room

– purchased house or apartment

– hotel or pension

– your old home, if for family reasons (there is a whole list of reasons) you move to an apartment that is far from work, and use your old apartment for overnight stays on weekdays.

It is specifically stated that Wohnmobil (camper) is not such housing. Which is strange, since they are rented out as rooms and such offers are not uncommon on Airbnb.

It is important that if you pay for housing, for example a room in WG, for six months, then during this paid period this room should not be rented further in your absence. This is formulated in such a way that housing must be at your disposal at all times

Requirements for first home

There are also requirements for the main housing: it must not lose the functions of the main one. In some cases, there are no problems: married people usually have no problems, especially when they have children and regularly return home (2 times a month for trouble-free filing of the declaration, at least 6 times a year with verification). The “center of vital interests” and “participation in the maintenance” of the first home in such cases is automatically recognized by the tax authorities.

Difficulties may arise in the following cases:

– you are alone and live with your parents. Here you will have to prove that you spend your money (at least 10 percent) on maintaining this home and that you have some social interests there (for example, you go to a sports club on weekends, go to doctors, have a partner). Tax office (Finanzamt, FA) prefers to see regular spending rather than occasional ones

– unregistered spouses are also recommended to have evidence of financial participation in the maintenance of the apartment (rent, Nebenkosten, electricity, food) and social life in this place

– cases when people move to another home, making the old one their second, periodically end up in the courts, so they need special attention

– another problematic case: your family lives abroad and you cannot travel there often. In these cases, one trip home per year is enough, but, most likely, the tax authorities will check financial participation and social life

– if you are planning to get a divorce and therefore have a second home, it will not be recognized.

If you feel that the tax authorities may not recognize your second home, it is better to contact a tax consultant, since we are talking about significant amounts.

Deductible expenses for second home in declaration

For employees, this is part of Anlage N, so we start line numbering at line 91.

Of course, you cannot deduct everything that your employer compensated you.

Fill in Anlage N:

Tax return in Germany. Elster online. Anlage N. Working expenses

Anlage N and costs of way to work

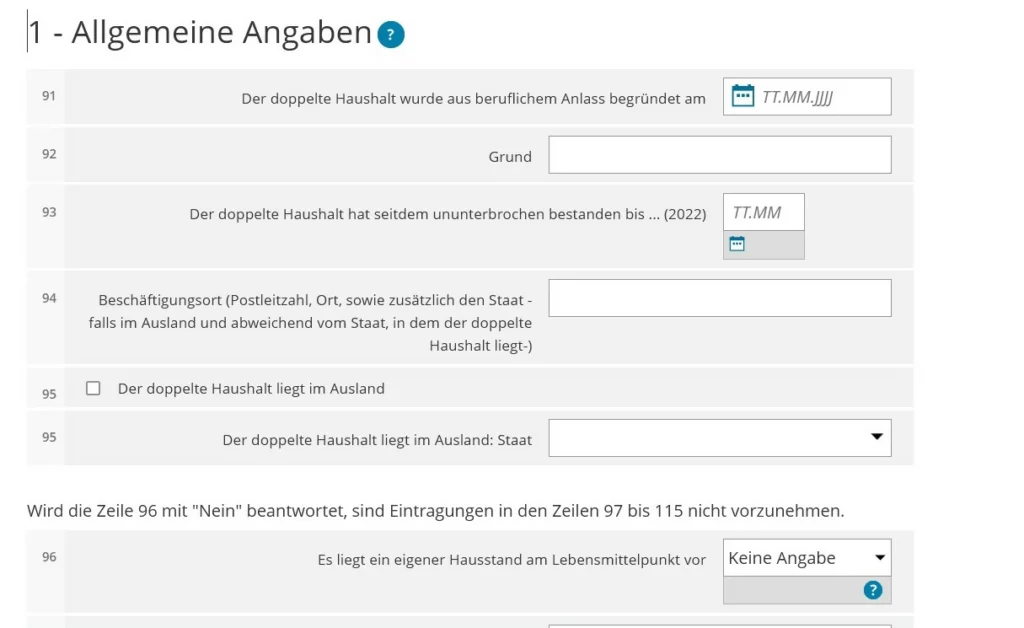

Section one – general information

In line 91, enter the start date of the “foundation” of the second home.

Line 92 contains reasons, for example:

– job change

– transfer of organization

– transfer of you as an employee to another department (Versetzung)

– you change your main home, turning your old one into a second work home (Wegverlegung)

In line 93, you must indicate until what date in the declared year your second home was in operation without interruption. If you give up housing for more than 4 weeks in the middle of the year, your Doppelte Haushaltsführung is interrupted. You start a new one, and the three-month period in which you can deduct food expenses begins again.

Line 94 is the address of the organization where you work. Separately, line 95 is for those who have a job and a second home abroad.

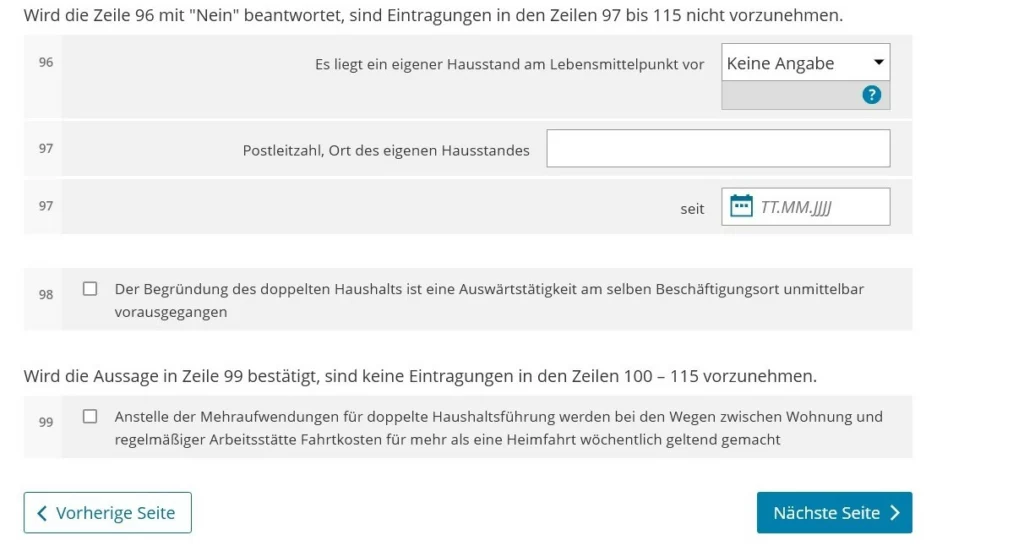

Lines 96-97 – your first home, its address and the date from which you have been running an independent household there.

One trip per week to your first home is taken into account for tax deduction. Line 99 is for those who travel more than once a week, who have counted all these trips and found that deducting all trips is more profitable than deducting housing.

Trips home are deducted at 30 cents for the first 20 km, then at 38 cents (one way only). Travel on public transport is limited to 4,500 euros.

This option (deduct trips instead housing) can be beneficial if housing is cheap and the distance is long, or if overnight stays were not made every time. Don’t forget that in this case you cannot deduct other expenses, only travel expenses. In addition, employer surcharges for travel or housing, if any, will be deducted from this amount.

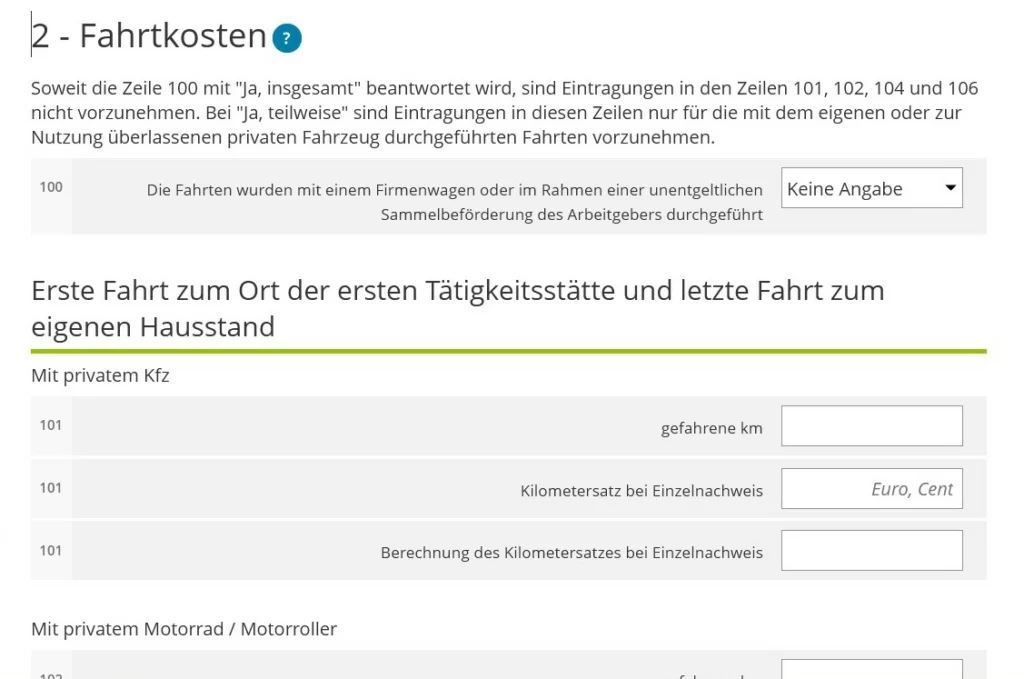

Section 2. Travel expenses

On line 100, you indicate whether the organization’s transport or a “joint delivery” organized by the employer was used for travel.

Lines 101-105, 106 will only take into account trips using your own transport, when you were not delivered and the employer’s transport was not used.

Line 101 – how many kilometers you drove on your first and last trip to work and back. Unlike trips home, which are listed further, this trip is deducted at 30 cents per km (20 cents for motorcycles) regardless of the number of kilometers, but it counts as a round trip.

It was unexpectedly unpleasant: having to prove that trips home really took place. Despite the fact that the hotels were not booked for the weekend, that is, the person was clearly in another place. If you have an apartment booked for a long period, then the need to prove travel home is even more obvious. You can prove it with a verified mileage meter. We had annual technical inspections in the garage.

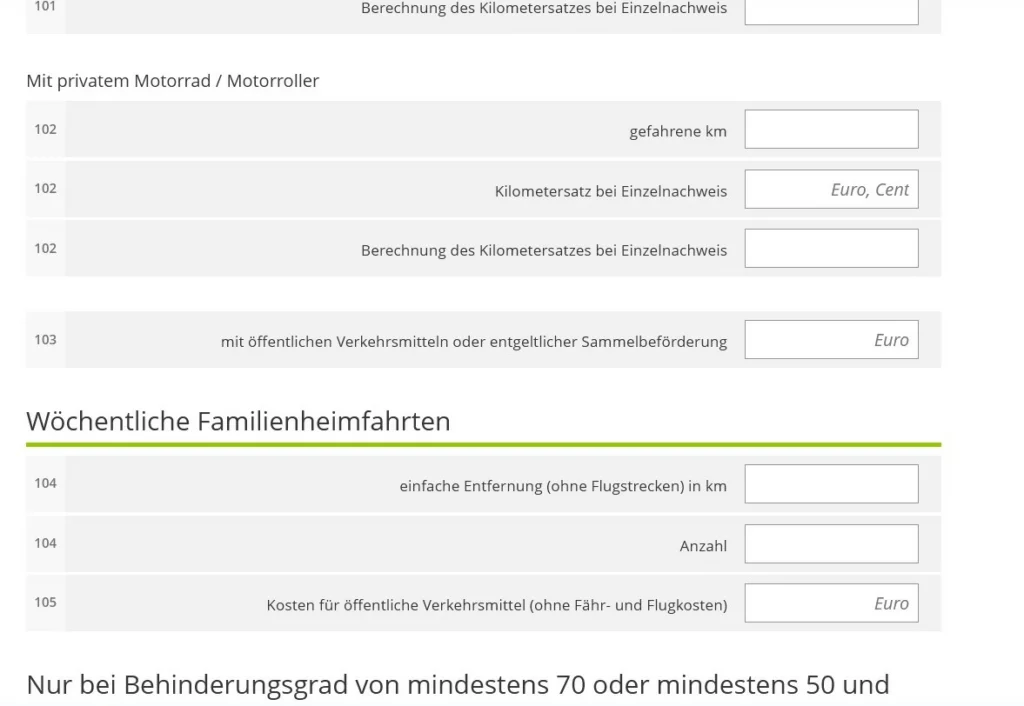

Lines 102-103 are for those who used a motorcycle.

Line 104 – distance (one way, the shortest route) in kilometers from the second place of residence to the first and the number of trips per year. You can only count one trip per week and a maximum of 33 trips per year. The first 20 kilometers will be counted at 30 cents per km, the rest at 38 cents per km (from 2022).

Instead of a trip, you can consider a telephone conversation.

Line 105 – the cost of travel if you used public transport other than an airplane. Plane and ferries – in line 108.

Deductible expenses for second home

All expenses must be provable. We will have two types of housing expenses:

– expenses directly related to housing

– associated costs

Expenses directly related to housing:

- rent

- or payment for a hotel room. No food. If breakfast is included but not separately listed on the invoice, you must deduct from the price:

for breakfast – 20 percent of the 28 euros (meal allowance) multiplied by the number of days with breakfast (that is, if there were four days, then 5.6 * 4 =22.4, rounded 22 euros minus),

for dinner (if they were) – 40 percent of 28 euros.

- garage rental (parking fee)

- Nebenkosten, electricity

- cleaning fee

- garbage removal

- Zweitwohnungssteuer and Grundsteuer

- for those who bought this home, there is a whole list of other expenses, some of which need to be written off gradually (writing off the cost of 2 percent, interest to the bank, etc.). In this case, I recommend contacting a specialist at least once to see how to deduct it correctly, because I have not seen any detailed analysis. Be sure to get a copy of your declaration right away.

Expenses of the this group are taken into account no more than 1,000 euros netto per month (averaged over 12 months, that is, no more than 12,000 per year if you had a second home for a whole year).

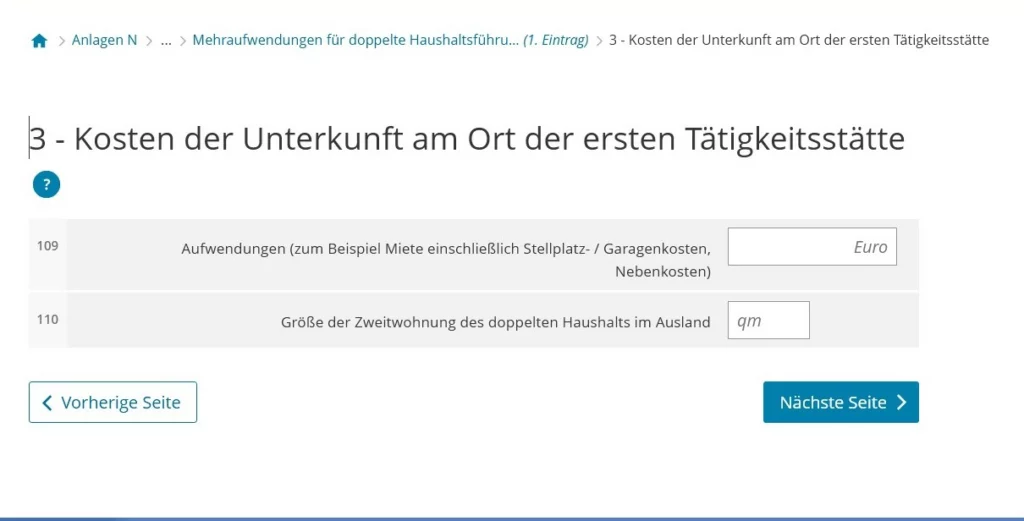

In line 109 we indicate the amount of expenses from the first group for the period of use of the second home. Line 110 for those who worked abroad.

The line implies the total amount of expenses. But the FA will definitely check it point by point. Be prepared to submit papers for each expense and make a list in advance.

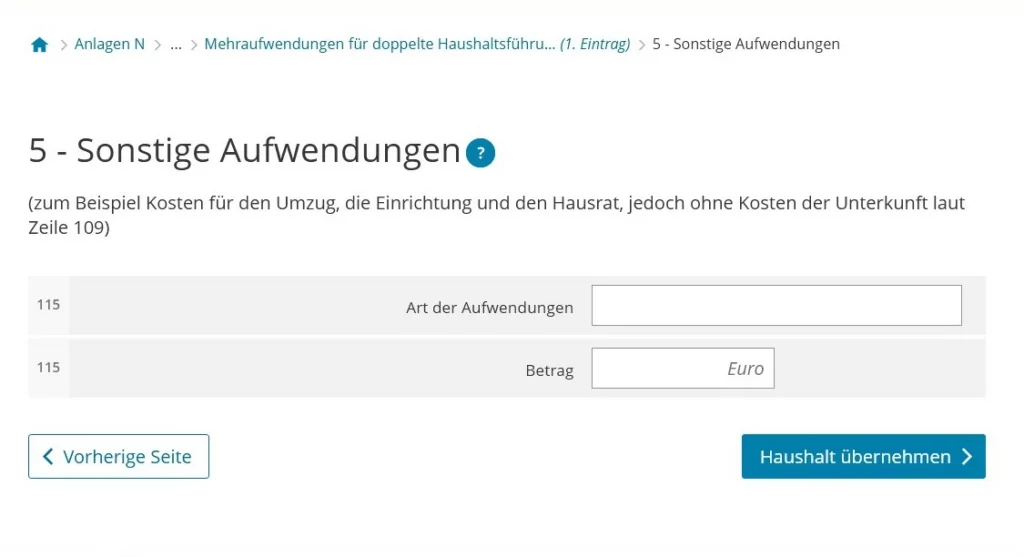

Second group of associated costs:

- broker fee for searching for housing

- expenses for home visit (travel costs)

- moving expenses (payment for transportation assistance, transport, packaging) – in actual amounts spent, without lump sum

- cost of repairs (painting, wallpaper)

- purchase of necessary things (kitchen, refrigerator, washing machine, bed, bedside table, wardrobe, table, chairs, bathroom equipment, curtains, lamps, dishes)

The second group of expenses is indicated in the last section 5 Sonstige Aufwendungen.

Expenses for the purchase of items can definitely be deducted in full (that is, above the 1000 per month limit), but some of them may require write-off over several years (if the cost of the item exceeds 800 euros net, that is, 952 euros gross). The write-off period for furniture is 13 years.

The FA accepts up to 5 thousand expenses without thorough checks. The costs above will already be studied.

I haven’t found out whether repairs are subject to the limit of 1000 euros per month or if they are taken into account separately. The practice of application is formed by court decisions and some things can be said unambiguously, since there is a court decision, but some things are not said unambiguously. The courts examine every item, right down to the TV (which, by the way, is not deductible).

Moving expenses in the case of Wegverlegung (when it is not the second apartment that is being sought, but the first one being moved) may not be accepted, since in one of the court decisions this move was considered private.

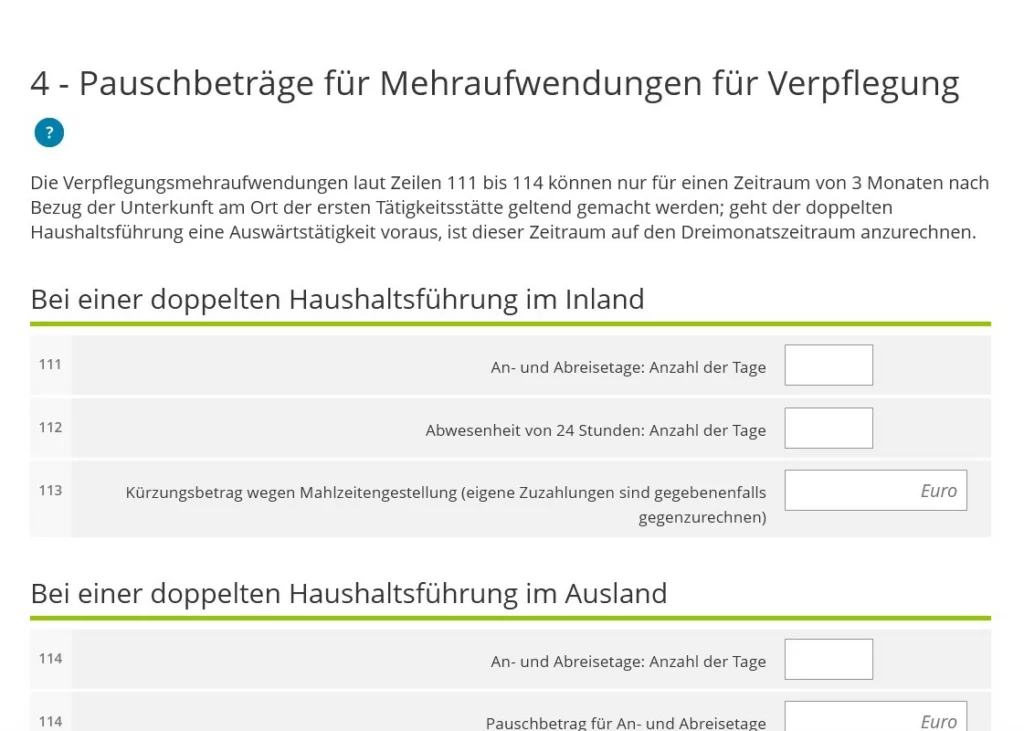

Paushal for food expenses

Food expenses are deducted during the first three months of life with two homes.

The days when you arrive or leave (stay in the first apartment for less than 16 hours) are charged 14 euros per day (16 euros in 2024, to be checked every year). Line 111.

Days when you are at your second apartment/work full time are valued at 28 euros per day (32 euros in 2024, to be checked every year). Line 112.

If you were at the first apartment for more than 16 hours and only went to the second apartment in the evening, these days are not counted for paushal.

Once again I would like to remind you that if your case is not the simplest: you need to justify the center of vital interests in the first home, or the family is abroad, or the second apartment is owned, etc. – it’s better to contact a specialist, since often we are talking about returning some thousand euros and the costs of a specialist will be justified.

Who should file a tax return in Germany

Home office tax deduction in german tax return

Elster online. 6. Household works deduction – Anlage Haushaltsnahe Aufwendungen (35a)

Tax return in Germany. All income tax deduction P-W

German tax refund – What I can claim to return. I-N

Tax return in Germany. Elster online. Anlage N. Working expenses

Pre-filled declaration in Elster

German income tax declaration. Anlage N-Aus

Tax declaration Germany. Anlage EÜR

How to calculate tax in Germany. What is written in Berechnung in Elster

Do you enjoy the site without cookies and maybe without ads? This means that I work for you at my own expense.

Perhaps you would like to support my work here.

Or Cookie settings change: round sign bottom left