Last Updated on September 27, 2023

Next part of income tax deduction in German tax return, among them the most important – deduction of expenses for work.

Not forget: außergewöhnliche Belastungen (Exceptional costs) are deducted, if they over individual limit.

How to calculate the limit of außergewöhnliche Belastungen read here

Other parts: A-D, E-H, I-N

Quick navigation

pets

pregnancy and birth

private school

profeccional illness

property

renovation

renting house maintenance

sanatorium

semester abroad

tax consultant

travel card

tutoring

vaccination

works expenses (Werbungskosten)

way to work

way to hospital

Pets

Most of the expenses for pets, such as food, toys, care products, houses, etc., are not deducted in any way. The same goes for vet and tax. An exception is animals used for work: all costs for them can be deducted as Werbungskosten.

In relation to pets, deducted are:

– expenses for compulsory insurance (goes along with other compulsory insurances in the amount, that is, most likely it will not be taken into account, since the maximum is quickly chosen)

– the cost of maintaining the pet at home (shearing, looking after while you are on vacation – both on your territory) – as Dienstleistungen.

About Anlage Haushaltshane Aufwendungen.

Pregnancy and birth

As außergewöhnliche Belastungen can be deducted:

- bills from Hebamma and the cost of medicines and examinations that are not paid by the Krankenkasse, but are prescribed by a doctor

- childbirth preparation courses

- gymnastics before childbirth (if prescribed by a doctor), gymnastics after childbirth

- fare for examination, gymnastics or preparation courses for childbirth and childbirth (when traveling by your own car at 30 cents per km)

- hospital stay that is not compensate by Krankenkasse.

- Items for children or mothers, the cost of freezing cord blood is not deducted.

Private school

The fees for a private school in Germany or abroad (in Europe) may be deducted if, upon graduation, the student receives a certificate recognized in Germany. Up to 30 percent of the payment is deducted (maximum 5000 per year) – as Sonderausgaben (indicated in the Anlage Kind).

Anlage Sonderausgaben.

Anlage Kind

Food and accommodation, materials are not written off.

School fees, donations are written off.

If the child is attending school for therapeutic reasons (has a corresponding recommendation), then more costs can be written off – as außergewöhnliche Belastung.

Profeccional illness

If you have an professional disease (list: gesetze-im-internet.de/bkv/anlage_1. html) or are the victim of an accident at work, treatment that was not covered by the Krankenkasse can be written off to Werbungskosten.

Read more about Werbungskosten in Anlage N

Follow me

Property

A loan for the purchase / construction of real estate can reduce taxes if the real estate is purchased for work purposes, for renting or as a second work apartment (in this case, no more than 1000 euros per month for all expenses on the second apartment).

Renovation

Renovations in the house you live in are deducted as Handwerker in Anlage haushaltsnahe Aufwendungen (20 percent of the cost of the work).

About Anlage Haushaltshane Aufwendungen.

Repair in the second “working” apartment – as Werbungskosten.

Rented apartment renovation – as Werbungskosten.

Read more about Werbungskosten in Anlage N

Renting house maintenance

Rental income is subject to taxation, but a variety of expenses can be deducted from it:

- furniture for a furnished apartment, items like sockets, switches, etc. (items more expensive than 800 euros netto (until 2018 – more than 410 euros) are written off gradually.

- costs of house or apatment (housing built before 1924 – 2.5 percent per year, after 1924 – 2 percent per year until 100 percent is selected)

- Grundsteuer

- interest on a loan

- account maintenance costs

- broker costs

- advertising

- if there is no broker, then the costs of registration and search

- Nebenkosten

- renovation

- reconstruction

- way to apartment

- the cost of a lawyer

- membership in renting associations

- the cost of paying the tenant to move out (in case there are plans for an reconstruction or sale)

- costs of empty apartment (you need to prove that the apartment is due for rent – renovations are being carried out, advertisements are printed, a broker is hired, otherwise the costs of long-term emptiness of the apartment will not be deducted)

Sanatorium

Travel and stay costs in the sanatorium (if not paid by the cashier) can be deducted only when there is a prescription from Amtsarzt that treatment in the sanatorium is necessary. The exceptions are cases when the sanatorium is partially paid by the Krankenkasse, then the Finanzamt considers that the Krankenkasse has already verified the need for sanatorium treatment. If the patient chooses not to live in the sanatorium itself, but in apartment, then the treatment must necessarily take place under the supervision of a doctor, otherwise the Finanzamt will consider it a holiday.

After subtraction the amount paid by the Krankenkasse or the employer, you can deduct from taxes:

- expenses for doctors and medicines

- massage, baths, etc.

- resort tax

- the cost of obtaining a certificate from a doctor

- cost of living

- tips –

- fare

- cost of care

To deduct the cost of a sanatorium for a child, you need to:

- the need for a sanatorium has been determined by Amtsarzt or the Krankenkasse

- the child at the resort lived in Kinderheim #

- treatment was carried out under the supervision of a doctor

As a rule, the Krankenkassen take the cost of the child’s stay in the sanatorium on themselves. The cost of an escort for one adult (travel and accommodation) is deducted only if the need for an escort is recognized by the district doctor.

Where: außergewöhnliche Belastungen

Semester abroad

Can be deducted

- cost of registration of applications

- the cost of a language test

- cost of education

- the cost of literature and office supplies

- cost of the road

- cost of living

- interest on student loan

- Verpflegungsmehraufwand

- medical insurance abroad

Education for the first specialty (bachelor’s and second education lasting less than a year) is written off as Sonderausgaben up to 6,000 euros per year. Second education, practice – as Werbungskosten.

Read more about Werbungskosten in Anlage N.

Anlage Sonderausgaben

Tax consultant

Tax consultant costs can be deducted if it is:

- advice on Werbungskosten for employees, people who rent housing, those who receive income from capital, rent

- accounting control and similar expenses

- everything related to professional activity

Cannot be deducted:

- costs of filing a tax return as a whole or separately Sonderausgaben and außergewöhnlichen Belastungen

- advice on income tax rates

- advice on deducting of help with the household

- inheritance and donation

- and other consultations related to the private (non-professional) life

In practice, this means:

Steuerberater must submit a separate invoice,

LoHi and tax programs are debited up to € 100 without separating work and personal expenses. If the amount is between 100 and 200 euros, then 100 euros will be debited. If the amount is more than 200 euros, then half is debited.

Read more about Werbungskosten in Anlage N.

Anlage Sonderausgaben

Travel card

The pass is counted in the Werbungskosten if you use it regularly for travel to work and if the purchase of the pass is more profitable than a day’s tickets in a month. However, if you are a self-employer, then it is difficult to deduct the travel card.

Read more about Werbungskosten in Anlage N.

Anlage Sonderausgaben

Tutoring

– only with other expenses for moving for work reasons, if the child, due to a change in school, had to turn to a tutor – in Werbungskosten

– or if the child suffers from dysgraphia or dyslexia (Legasthenie) – außergewöhnliche Belastungen

Vaccination

Vaczinations are deducted as außergewöhnliche Belastungen, if they are recommended by the doctor and are not compensated by Krankenkasse.

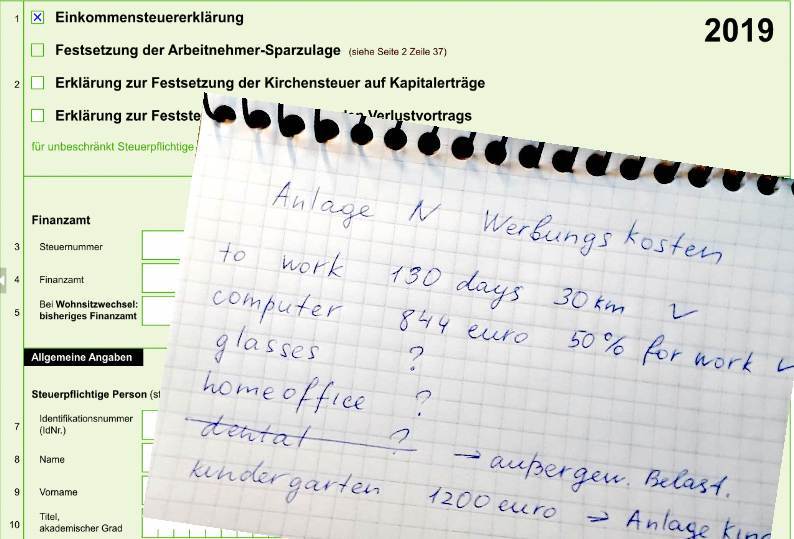

Works expenses (Werbungskosten)

They can be both for employees and for self-employer, part-time pensioners, those who rent out housing.

Werbungskosten are:

- way to work

- business trip (if not compensated by the employer)

- work clothes

- educational books

- tools

- equipment of a working room in the house

- home office (for 2020 and 2021 – read in separate post.

- second apartment from work purposes (dual houskeeping)

Read about dual houskeeping (Doppelte Haushaltführung) here. Read about home office here.

- re-education or additional training

- second education

- the cost of searching a new job (sending letters, travel, hotel accommodation)

- cost of moving for work reasons

Read more about moving for work reasons

- expenses related to an accident at work or on the way to work –

- fees to the union

- account management – pauschal sum 16 euros, does not require proof

- legal assistance in quarrel with the employer

- expenses for professional diseases

- tax consultation on Anlage N (only as an employee).

List of things, that were bought for work and are writted off gradually (limit – more than 410 euros netto until 2018, more than 800 euros netto from 2018).

In addition to the separate write-off, Poolabschreibung can be beneficial for items between 251 and 1000 euros. It lasts 5 years, 20 percent every year. The pool must include all items of the specified value purchased during the year.

Read more about Werbungskosten in Anlage N

Way to work

Travel expenses to work are deducted in the Werbungskosten. To track travel expenses, it is important how many kilometers to work, how many days you were at work and what kind of transport you get.

Way to hospital

If the travel to the place of treatment is not paid by the Krankenkasse, then it can be written off at the außergewöhnliche Belastungen. If you use your own car, then 30 cents per kilometer there and back are deducted. Treatment must be prescribed by a doctor.

All I can return from tax: A-D, E-H, I-N, P-W

Anlage N Part 1, Part 2, Anlage N-Aus, Anlage Wa-Est, Homeoffice

Anlage Kind

Anlage Vorsorgeaufwand

Anlage Sonderausgaben

Anlage Haushaltnahe Diensleistungen 35a

Who should file a tax return in Germany

Pre-filled declaration in Elster

How to calculate tax in Germany. What is written in Berechnung in Elster

Freiberufler in Germany: how to fill in Anlage S and Fragebogen zur steuerlichen Erfassung

Do you enjoy the site without cookies and maybe without ads? This means that I work for you at my own expense.

Perhaps you would like to support my work here.

Or Cookie settings change: round sign bottom left